In this piece, we delve into the emerging blockchain and non-fungible token (NFT) applications that are shaking up contracts and rights and royalties' models. We also explore how disruptors and incumbents are gearing up for the future - including a whole new digital world in the metaverse.

Challenges and friction in today’s media marketplace

In the first two articles of this Rights and Royalties series, we discussed how the forces reshaping the media industry are turning rights and royalties into a competitive differentiator, and the evolution of content creation. Here's a quick recap of the top five challenges impacting media organisations today:

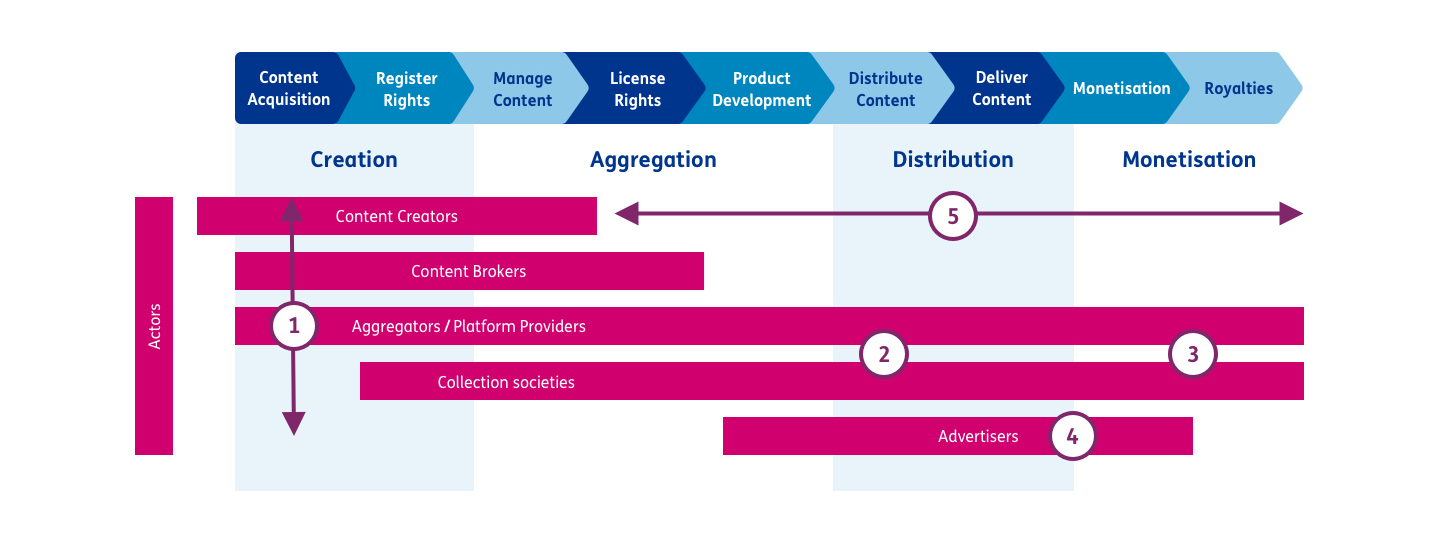

Rights and licensing complexity - Many media organisations have acquired intellectual property (IP), gone through mergers, or begun producing original content. On top of this, there are now more parties involved in commissioning, creating and licensing content. All of this means that media businesses are managing a more complex set of IP rights than ever before.

Challenges in tracking distribution and fighting piracy - Globalisation, streaming and expanding consumption channels - including syndication and social media - have driven a massive expansion in the volume and complexity of distribution that companies need to manage and track. This also makes it harder to crack down on piracy.

Managing content monetisation and calculating royalties - Media organisations are finding it harder to track content monetisation and calculate royalties quickly and accurately, thanks to the intricacy of IP rights and royalties rules, the inaccuracy and inefficiency of distribution data, and the disconnect between rights, distribution and financial processes.

Advertisement targeting constraints and ad fraud - Poor visibility into customers' content usage data makes it hard to precisely target ads to specific user groups. What's more, unreliable distribution data causes disputes between distributors and advertisers.

Creators' pay and reliance on intermediaries - Digital platforms like YouTube and TikTok have removed barriers to entry for aspiring content creators, galvanising a flourishing creator economy. Yet, creator frustration and resentment are growing. Creators want more direct-to-consumer options and far more equitable allocation of revenue from intermediaries, who can charge significant commission and provide limited insights into content distribution.

In this article, we'll explain how companies, creators and consumers can thrive in this exciting new era of media and entertainment by addressing their rights and royalties challenges using distributed ledger technologies or DLT - peer-to-peer systems that allow participants to simultaneously interact and transact within a secure, transparent, and immutable data network.

The future has arrived

Whenever a ground-breaking innovation emerges, there are sceptics and enthusiasts. For instance, a few years ago, the potential for distributed ledger technologies like blockchain was up for debate. But now, these technologies have become established across many fields and use cases, including decentralised finance, cryptocurrencies like Bitcoin, supply chain audit and digital identity. The UK Government Treasury this year announced plans to test DLT to become a global 'cryptoasset technology hub1.' Furthermore, investment in DLT use cases worldwide is forecasted to rocket from around $4 billion in 2022 to $140 billion in 20302.

Among this immense growth potential is a huge, largely untapped opportunity for the media industry, where DLT and blockchain technology could create a revolutionary shared, trusted and efficient transaction system for media assets.

Take NFTs, which became a phenomenon in 2020, was voted as the Oxford word of the year and rose to become a $4.4 billion market in 2021. Some were quick to ridicule them, and with fair reason, as most of the early collectible digital art NFTs were hijacked or originated as investment vehicles. Now we're seeing a renewed focus on the utilitarian design and potential of NFTs and smart contracts, which are based on blockchain and can execute interactions and transactions automatically once predefined criteria are met. Some estimates suggest the NFT market will reach a whopping $20 billion by the end of 20283.

Media organisations are gradually beginning to understand how DLT, NFTs and smart contracts will have an enduring impact on their business operations. Let's explore some of the potential use cases, and discuss how they tie into a broader vision for the future - including Web 3 and the metaverse.

Media industry applications for DLT and blockchain technology

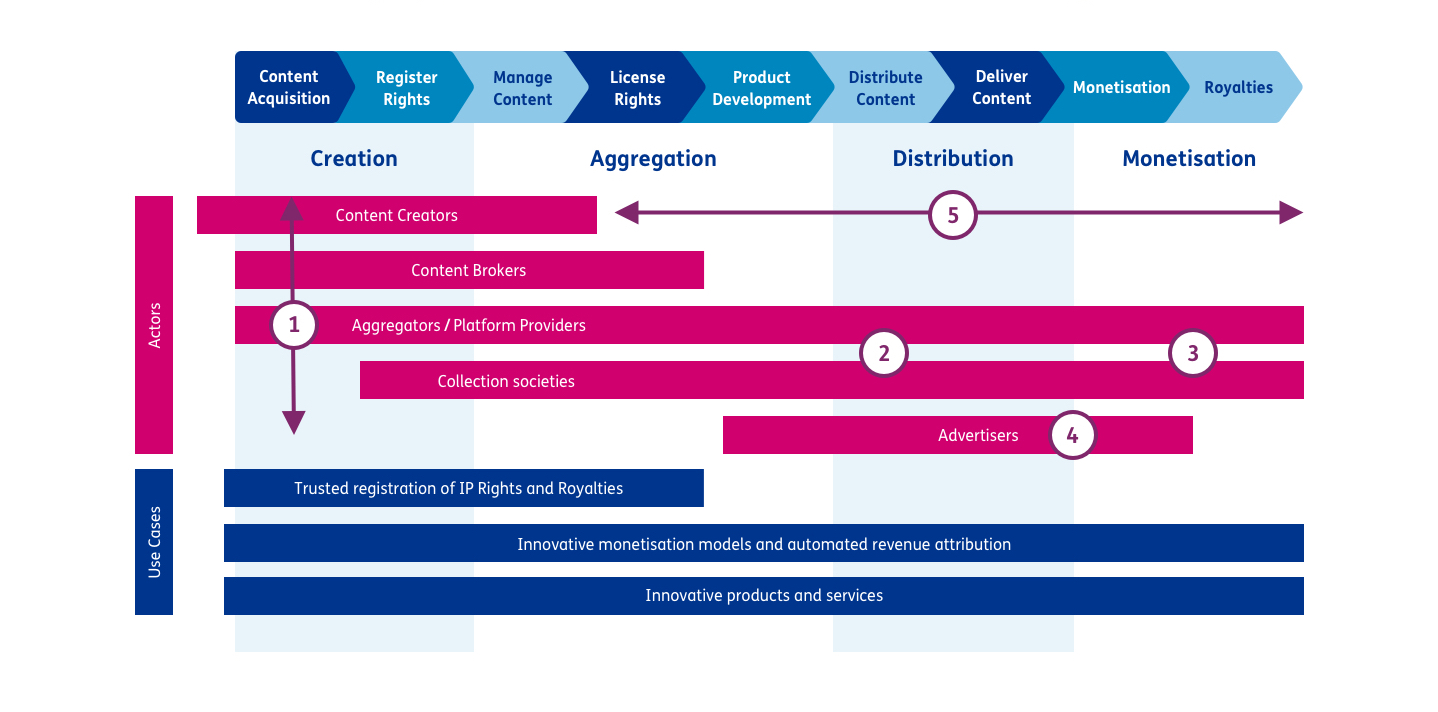

1. Enabling trusted registration of IP rights and royalties

Works, IP rights ownership, royalty rules and licensing deals are often stored locally across different parties in the media value chain. This creates a lack of transparency and data inconsistencies that require reconciliation and often lead to disputes. All of this contributes to inefficiency, inflated costs and lost revenues.

Blockchain can change all that. It can unify IP rights systems across industries and countries, vastly improving transparency, enforceability and efficiency. IP owners can register their works on an immutable shared ledger which acts as an authentication tool to validate the integrity of intellectual assets. Blockchain can also track and facilitate the exchange or transfer of IP assets and licensing using smart contracts.

Examples:

The European Union (EU) is developing a blockchain-based IP registry and supply chain tracking system to combat counterfeit goods. Due for full-scale rollout in 2023, it's one of the most ambitious blockchain projects to date.

Binded- Photographers upload their images to a copyright vault secured by a unique fingerprint saved on the blockchain. Once uploaded, artists can share their work and track similar images to thwart copyright infringements.

RightsfuAlly - Creators register scripts and films, then share them - for example, with third parties involved in movie production. The network provides complete traceability and transparency of who can access each document.

2. Innovative monetisation models and automated revenue attribution

Blockchain can dramatically simplify and accelerate royalties calculations, by providing transparency of content distribution. Furthermore, smart contracts can automatically enforce contractual agreements between creators, producers, publishers and advertisers in the media supply chain. This enables immediate and automated royalty and revenue share distribution at the point of sale or content consumption. The upshot is that media companies can pay creators in seconds instead of years, creating greater incentives for loyalty.

Self-sustaining solutions like the Flixxo example below could potentially eliminate the need for services and processes currently provided by content brokers (eg music labels and publishers), aggregators (like Spotify or Audible) and collection societies (which make sure creators get paid when their work is used). This is an attractive proposition for creators, who stand to gain more direct-to-consumer (D2C) relationships and greater revenue share.

With accurate, real-time tracking of content distribution enabled by blockchain, you can also:

Prevent piracy and revenue leakage – making it easier to identify when copyrighted material is used without permission.

Introduce per-use payment models – automation and much cheaper content distribution and monetisation unlock the potential for per-use payment models. These are ideal for consumers who want access to select pieces of content. For example, with a blockchain distribution model, creators or distributors could sell per-stream videos or per-read articles with instant distribution of royalties or revenue.

Establish customer-to-customer (C2C) models – onward distribution of acquired content is a longstanding source of revenue leakage in the media industry. But all that could change with smart contracts, which are associated with content assets in perpetuity. This enables new models whereby, for example, the original artist collects a share of revenue for all future transactions.

Enhance ad targeting and efficacy – because tracking content distribution is so challenging, media companies and advertisers often end up disputing the number of genuine interactions with ads. Smart contracts could change that, because they provide accurate, trusted tracking of users. Just as smart contracts automate the distribution of royalties, they can precisely collect and distribute advertising spending – avoiding arguments and fraud.

Examples:

Opus - Artists store their tracks on the Opus platform and music is streamed via the Opus player on the Ethereum blockchain. The blockchain-based revenue system provides artists with 90%+ of revenue vs ~20% on other platforms.

Flixxo - is a decentralised content distribution platform where audiences pay creators cryptocurrency tokens in exchange for their content. To earn Flixxo tokens, participants make the videos on their computers available to the network. This decentralised crowdfunding and peer-to-peer hosting solution offloads the cost of running the network onto the users – rather than platforms footing the bill and taking hefty commission. This makes it far more lucrative for creators to take part.

3. Innovative products and services

Over the past two years, NFTs have emerged as a product and service category representing the ownership of physical and, importantly, digital assets. When NFTs first emerged, many people saw them as gimmicks, as some pieces of digital artwork grabbed headlines by selling for staggering sums. And arguably, the NFT space was dominated by people trying to make a quick buck – with no serious thought about the technology’s wider implications.

Fast forward to today, and things have changed – particularly since the recent NFT market crash. Some people will see this as justification for their long-held scepticism around NFTs. But it could actually be a good sign of the market maturing and stabilising after the initial hype. For instance, remember the public reactions when Bitcoin crashed a few years ago? Compare that to today, when major economies are introducing central bank digital currencies (CBDCs), which are also based on DLT.

As the initial buzz dies down, we can have sensible conversations about the enduring use cases for NFTs in the media and entertainment industry. In this section, we explore the ones we believe are most promising.

Content and collectible ownership

There are several reasons why creators and companies are experimenting with NFTs in the collectible marketplace:

NFTs are unique. So savvy creators or distributors can create supply scarcity – and therefore desirability – by releasing only a limited number of them.

NFTs show their previous ownership history, and assets formerly owned by famous people are likely to fetch higher prices.

Crucially, unlike physical assets, NFTs are programmable. For example, they can ensure artists receive revenue throughout the lifetime of a work

Examples:

CryptoPunks – The first widespread NFT experimentation in mid-2017 consisted of 10,000 unique collectible digital punks. Each has a set of algorithmically chosen characteristics, a commonly used means to express rarity.

Muse NFT album – Muse made chart history by becoming the first act with a UK number-one album sold in the form of an NFT. The rock trio achieved the feat with their ninth album, Will of the People, which was released in the form of a limited-edition NFT as well as traditional formats.

Book.io – An NFT marketplace for buying, reading and selling eBooks and audiobooks. Authors get 70% of revenue from the initial sales, and further revenue when their work is resold. Readers can earn $BOOK tokens based on their amount read – incentivising them to become more deeply involved in the platform.

NBA Topshot – Launched in July 2019 as a digital reproduction of traditional trading card culture, NBA Top Shot was ahead of the curve from the start. Now, cards in high demand have an average sale price of $68,000.

Resourcing of creator projects

Just like companies issue shares, creators often fund their projects by selling shares of their work to fans and investors, who receive a proportion of revenue. Now, they can issue those shares of copyright ownership as NFTs.

NFTs can also represent membership in creator squads, where each production team member owns an NFT that gives them a share of the works.

Examples:

Royal.io – In 2022, rapper Nas released two songs with NFTs granting streaming royalty rights. A $50 ownership interest earned 0.0143% of the songs’ streaming royalties, while a $4,999 purchase netted 2.14%.

Opulous – A platform that connects artists with investors and offers NFT purchasers a share in the music copyright, which generates monthly revenue as the project progresses.

Squad of Knights – Lets its NFT owners form six-person squads, with each person assigned a role in the music production process. Unlike traditional record labels, the platform lets community members own 100% of the music they produce.

Fan club membership

Similar to the above examples, creators and media companies can sell NFTs granting membership to exclusive fan clubs that offer real-world benefits.

Examples:

Paris Saint-Germain (PSG) fan token – Ownership of the NFT grants access to limited and signed merchandise, VIP tickets, and even voting power on club decisions.

Corinthians via Socios.com – A rugby team’s NFT that gives owners the right to vote on the colour of the club’s next uniform, and the locations for friendly matches. In the future, it could give them a share of ownership of stadiums and training grounds, or let them participate in appointing new coaches, chairpersons or managers.

Coachella NFT – Coachella festival’s collectible NFTs are a first-of-their-kind opportunity to own lifetime passes, unlock unique on-site experiences, physical items and digital collectibles.

In-game assets and new types of metaverse content and worlds

Long before NFTs, the gaming industry created in-game economies for digital assets like playable items or ‘skins’ – stylised outfits for characters. Now, DLT has spawned a new generation of games that formalises in-game economies and ownership of digital assets.

This has culminated in the evolution of the metaverse – virtual worlds built by consumers, creators and companies. Blockchain-based platforms can be used to create ‘decentralised’ VR worlds that are owned and managed by the community of users who inhabit them.

Examples:

Axie Infinity – A player-owned economy where players have ownership of their digital assets and can buy, sell and trade NFT monsters and pit them against each other in battles. It’s part of a category of ‘play-and-earn’ games, where players can earn resources with monetary value from gameplay.

Decentraland – This digital 3D virtual reality world based on the Ethereum platform is an open metaverse – one that anyone can enter. It allows users to be part of a shared digital experience in which they play games, buy and sell digital real estate, create and exchange digital assets, and interact with each other.

Audius - A decentralised repository of content that lets metaverses provide music to their users. Creators are rewarded with Audius tokens. Users can also earn tokens by curating successful playlists. And thanks to clearly defined rights, third-party developers can pull from the platform’s catalogue without any issues.

Hurdles to overcome to make these applications highly scalable

It’s clear that DLT and NFTs offer huge potential for the media industry – particularly as the technology matures and organisations collaborate on new possibilities. We expect to see many more of these applications coming to life and scaling in the next three to five years.

To capitalise on these opportunities, industries are working to overcome hurdles that prevent mass rollout and adoption of applications, including:

Industry standards: Membership organisations like the Digital Data Exchange (DDEX) strive to establish standards around how they communicate information about works, tracks and products – including ownership and sales information – so each party receiving the metadata can understand it. The same concept applies here. Common industry standards would be needed for DLT(s) to manage contracts, rights and royalties at a global, industry-wide scale.

Governance requirements: In the use case for trusted registration of IP rights and royalties, if the DLT platform were decentralised and permissionless, anyone could write to the ledger and there would be no means to change data if somebody entered incorrect information. This needs to be considered in future models, where a suitable governance model or authoritative third party would still need to be involved.

Transaction volumes: Many applications are held back by the volume of transactions that current blockchain technologies and protocols can handle. For instance, Visa can process up to 24,000 transactions a second, whereas Bitcoin can only process seven and Ethereum 20. To put that in perspective, Spotify's most-streamed song of 2021 - Olivia Rodrigo's driver's license - racked up 1.1 billion streams, whereas Ethereum can only track 600 million streams per year. For now, unless transactions are aggregated, this restricts DLT's content distribution applications to low-volume content consumption platforms.

Energy and sustainability: The energy requirements to run today's DLT networks are unsustainable. For example, Bitcoin consumes more energy than Norway each year. Ethereum is leading the charge by switching to a new 'Proof-of-Stake' protocol that could improve energy efficiency by up to 99.9%5.

Companies’ and creators’ trust in DLT technology and platforms: The DLT domain can feel technical. Without third-party advisory services, the barriers to entry for creators and companies are high. As the market is changing so quickly, it’s hard to know whether to use one of the existing DLT platforms or build your own. Furthermore, the volatility of NFT and cryptocurrency markets generates fear, uncertainty and doubt.

Friction for consumers: The world of DLT and NFTs has its own language. To delve deeper, consumers must understand terms like 'wallets', 'tokens' and 'gas fees'... User experiences will need to become less daunting if the platforms are to gain widespread appeal beyond an enthusiastic pool of early adopters.

Disruption and disintermediation – where are we headed?

We’re in the age of the tech platform monopoly. Spotify, YouTube, Netflix, Audible, social media platforms, digital content and streaming have galvanised a creative revolution. However, they’ve also introduced ever more intermediaries and positioned creators further from their audiences and points of pay.

Creators are losing patience, and resentment toward the power imbalance is growing. For example, music artists in the UK recently raised complaints about their low revenue shares with the Competition and Markets Authority (CMA), arguing that streaming “benefitted music companies and streaming services at the expense of the creators who sustain the industry.”6 Another example is electronic artist Four Tet, who recently won a royalties dispute with his former record label. He now earns 50% of royalties – far above the previous rate of 13.5%. And the label has agreed to back-pay around $70,000 in historical royalties going back to 2001.

We’re also seeing a huge increase in creators moving their fan bases off social networks and platforms to their own websites, applications and monetisation tools. Many are flocking to membership platforms like OnlyFans or Patreon, which have experienced exponential growth over the past three years. For example, the number of creators on Patreon with at least one patron has shot up to 220,000 – that’s 480% higher than in 2017. And the number of active patrons has increased by 50% over the last year to over 6 million7.

As the content creator economy matures and DLT opens up more D2C channels, more and more creators are jumping feet first into emerging use cases, like NFTs, to take back the power.

Taken to an extreme, if large-scale decentralised platforms are established, many of today's aggregators, platform providers, and collection societies could become obsolete. This is the vision for Web 3 - a new decentralised version of the internet, where users retain control over their data and content, and they can sell or trade their data without losing ownership, risking privacy, or relying on intermediaries. As with many of the use cases described, the new marketplace will be supported by the digitisation of assets via tokenisation. For creators, this represents a D2C marketplace with unlimited potential.

What does this mean for today’s intermediaries?

Only time will tell if this vision for the future will become a reality. But it’s clear that market dynamics are changing. Each actor in the media value chain should investigate how D2C and DLT use cases will impact them, and explore opportunities to strengthen their market position.

Emerging DLT applications like NFTs are meeting creator needs for fair compensation. However, intermediaries today provide more than just a marketplace. For example, Spotify isn’t just a way to stream music. It also offers smart search and recommendations, and community and sharing features. These capabilities and the network effects of platforms will continue to make existing market leaders resilient to disruption.

Content brokers, aggregators, and collection societies should refrain from living in fear, waiting for an extinction day that may never arrive. Instead, they can identify opportunities to incorporate DLT into their business strategies. For example, aggregators can use the technology, combined with user experience and personalisation services to position themselves as fairer partners to creators.

Once more use cases are proven, we may see others rush to implement and scale effective solutions, like the one implemented by the European Union.

What do we recommend?

1. Cut through the noise

Organisations need to stay close to the market and understand what the emerging strategies mean for the industry and their business model. Cutting through the sea of vanity projects and headline-catching coverage, it’s vital to know the core principles and value drivers to determine which developments will be persistent and which are just fleeting distractions.

2. Define your vision and DLT strategy

Organisations need to understand how DLT will affect their businesses, and form a strategy to address it. Will you look to seize early-mover advantage from DLT, or wait and see what happens? Will you partner, invest or acquire the capability? How will DLT sit alongside traditional models? Organisations should brainstorm ‘what if’ scenarios and create a vision for how this technology could either threaten or fit into their future commercial offering.

3. Prioritise use cases, learn and scale

Sometimes companies are quick to adopt new technologies to show they’re in touch with the future – but the projects themselves don’t necessarily deliver much value. To avoid this pitfall, each organisation must identify and prioritise use cases to explore. We recommend embracing a start-up mindset, starting small, working swiftly to build proof of concepts, and focusing on use cases that let you test applications in the real world. By failing fast and seizing the opportunity to learn, early movers will accumulate deep knowledge of the people, processes, system, and data facets required to be successful.

Conclusion: Prepare for the modern media marketplace

We’ve come to the end of our final article in our rights and royalties series. So, what have we learned?

We’re shining a spotlight on the profile of customers, businesses and sectors who have been most affected by vulnerability. We’re engaging with senior leaders to understand what actions can be taken to support customers and businesses proactively.

This is a challenge we really care about. We’re excited about developing the thinking across multiple markets and exploring what proactive actions can be taken to provide customers with the support they really need.

We’re experts in both of these domains and we’re hugely passionate about these topics. If you’d like to talk about these developments, what they mean for your business and how we can help, please get in touch.

Our Experts

Joe Selwyn

Partner, expert in Media and Tech-enabled Transformation

How can media companies transform their IP rights and royalties capabilities into a powerful competitive differentiator? Our media team share their insights.

Is digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?