State of climate reporting: Five observations on energy and commodities trading

5 December 2023

Baringa benchmarking shows that trading companies are expanding their climate reporting to meet evolving regulations and the demands from banks, shareholders, and investors.

Integrated oil & gas and mining majors have been reporting on their emissions for many years as part of their wider corporate social responsibility and sustainability agendas. Pure commodity traders, once laggards in this space, are increasingly joining them, as climate-related disclosures become a prerequisite for accessing capital markets and securing financing.

One of the main drivers for enhanced climate reporting have been regulatory frameworks such as the Taskforce for Climate-related Financial Disclosures (TCFD) which has been mandatory for large companies in the UK since 2022. Regulatory requirements are expanding: the new International Sustainability Standards Board (ISSB), which builds on TCFD, is expected to be made mandatory in other jurisdictions.

However, the real pressure to report is not coming from regulation but from banks and investors, who are increasingly demanding that traders, including privately-owned companies, align to climate reporting frameworks and provide greater transparency on the potential impacts of climate-related risks and opportunities on their financial results.

Climate reporting frameworks do not neatly apply to the complexity of trading activities and many traders are developing tailored approaches to measure, manage, and report their climate-related exposures. Baringa has performed a benchmarking exercise to review the climate disclosures of key players in the commodity and energy trading industry.

Observation 1: There is still a large variance in the approach and boundaries used for emissions reporting, especially when it comes to scope 3.

Most commodity and energy traders now report on their emissions on an annual basis – and importantly, most now include scope 3. This is significant because for asset-light trading organisations, or the trading arm of vertically integrated companies, scope 3 represents the majority of emissions.

For traders, scope 3 emissions will typically include emissions from:

-

Upstream supply chains, such as extraction, production, or manufacture of traded commodities.

-

Third-party logistics and transportation, such as chartered vessels used to transport a company’s products but operated by a third party.

-

Downstream emissions from processing and end-use of sold products, including combustion of energy products.

However, although traders are increasingly reporting on scope 3, there remains a huge breadth in the comprehensiveness of emissions reporting across the sector.

First of all, there is variance in terms of which categories are considered material and therefore included in reporting. For example, O&G producers that have trading divisions tend to focus on end-use emissions (cat 11), while pure trading organisations tend to report on a broader range of scope 3 categories, reflecting the relative importance of categories such as transport (cat 4 & 9) to their business activities. In contrast, purchased goods (cat 1) is the focus of most agricultural traders who are increasingly also incorporating land-use change emissions.

Secondly, and more importantly, the reporting boundaries used to determine what trades are included in scope 3 reporting vary significantly. The challenge for traders is that the GHG Protocol does not provide much guidance on how traders should report on emissions. The only relevant example in the GHG Protocol, which refers to power trading, suggests that only sales to end-users are compulsory and that other intermediate trading transactions can be excluded but there are no clear definitions of end-users or intermediate transactions.

This has driven the sector players to adopt a slightly different approach to defining their boundary. No players include 100% of gross sales in their scope 3 reporting. The approaches can largely be split into three camps, those who only include sales from production volumes (i.e., entirely exclude trading volumes), those who only include sales-to-end users, and those who have set mixed boundaries, including trading volumes for certain categories or certain products.

The lack of clear standards in the industry makes it difficult to compare ‘like-for-like’ and opens traders to accusations of greenwashing. To counter this, traders must clearly define their emissions measurement methodology and justify any exclusions.

Observation 2: Traders are increasingly setting emissions intensity targets. This makes sense but they must be underpinned by clear and credible transition plans to avoid greenwashing accusations.

Scope 1, 2 and 3 emissions are typically used to report on absolute emissions, reflecting the total amount of greenhouse gases (GHGs) emitted into the atmosphere by an organisation over a specific period. Traders, however, are increasingly also disclosing emissions intensity metrics, which reflect the amount of GHGs emitted for a given unit, such as grams of CO2 equivalent per megajoule or per tonne.

In many ways, intensity metrics are a better measure than absolute emissions for trading. Absolute emissions are highly sensitive to volume fluctuations which means that, depending on the boundaries used, they tend to be directly linked to the size of a trading book and can misrepresent the climate impact of trading. For example, an oil trading organisation could be penalised for increasing their participation in a high-volume market such as natural gas even if it has lower emissions per unit than other fossil fuels. Conversely, the same trader could meet absolute emissions targets simply by cutting down the traded volume in an unprofitable book without actually reducing their real-world carbon impact.

If used correctly, intensity metrics can be valuable tools to track progress against climate goals. They can be used to incentivise traders to trade lower carbon products by rewarding them for reducing their average emissions per unit of energy or mass traded. This also aligns with requirements from counterparts who may be interested in understanding the carbon intensity of purchased products. Indeed, green premiums are starting to develop in some commodity markets such as aluminium, where lower carbon intensity products can command a higher price. This will be strengthened by growing carbon taxation policies, such as the EU’s Carbon Border Adjustment Mechanism.

However, intensity metrics should not replace absolute emissions reporting and any intensity-based targets must be clearly linked back to broader decarbonisation goals. To avoid accusations of greenwashing, traders must be able to demonstrate to investors how they will use intensity targets to drive down real-world emissions over the short, medium, and long-term by steering capital flows to lower carbon products.

Doing this well is not easy, and it needs to be underpinned by accurate and meaningful data to avoid reliance on industry average emission factors which may not reflect the actual emissions of specific products or sources.

Observation 3: Climate risk reporting remains a formality. Banks and investors will require traders to do more.

Traders are increasingly including disclosures in their annual reports to align with climate risk regulatory frameworks such as TCFD (and now, ISSB). Designed to improve the transparency and accountability of climate reporting, these frameworks require companies to disclose how climate change affects their financial performance, strategy, governance, and risk management.

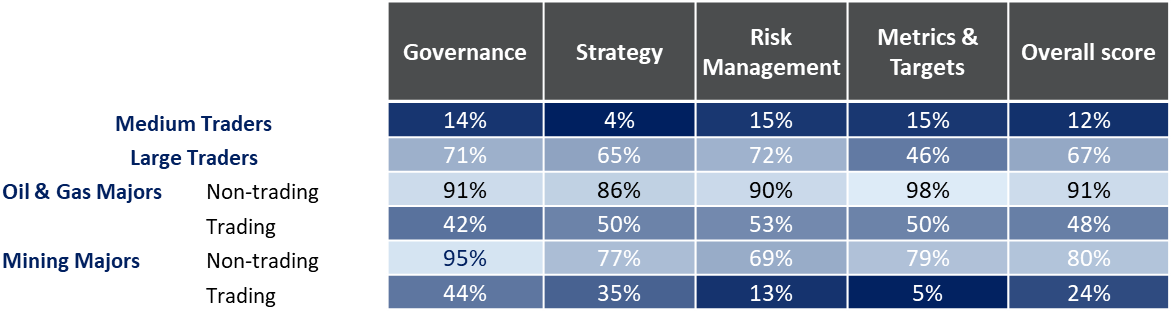

As part of our benchmarking, Baringa assessed the maturity of climate risk reporting in the industry against best-practice disclosure. We reviewed the climate disclosures of a variety of traders and assessed to what extent they met the recommendations for each of the TCFD/ ISSB pillars1:

The result of our benchmarking shows that the trading industry still reports on climate risk at a high-level and generally does not have the level of detail required to meet the growing expectations of investors and the financing community. Our benchmarking also showed that, for integrated companies, the trading arm is generally not as compliant to ISSB and TCFD standards as other parts of the same entity. It is more complex to apply climate frameworks to a trading business and, as a result, integrated firms often omit information on their trading activities.

Traders perform the least well against the Strategy pillar. This reflects the difficulty of the recommendations, such as the requirement to use scenario analysis to identify risks and assess strategic resilience, which is a challenging task (see observation 4). However, traders can enhance their disclosures without having to invest in complex scenario modelling. As a starting point, they can simply focus on analysing the impact of climate scenarios on key climate risks, such as physical risks for their assets, before building this out into more refined scenario modelling.

The introduction of ISSB, as well as growing pressure from banks, will drive increased compliance across the market. Baringa is expecting to see a significant increase in the breadth of climate reporting from trading firms from 2024 and onwards.

Observation 4: Traders must learn from financial services to incorporate climate scenario analysis into existing risk management practices.

Managing risk is at the core of commodities and energy trading but very few traders directly consider the impacts of climate change as part of their trading risk functions. Incorporating climate scenario analysis into existing risk management practices is not only needed to align with frameworks like TCFD and ISSB but done correctly, it can also help traders better understand and manage the potential impacts of climate change on their operations.

Climate scenario analysis, which is required under ISSB, can be invaluable tools for traders to stress test the potential financial impacts of climate scenarios on their portfolios. However, most traders still treat scenario analysis as a standalone sustainability requirement rather than incorporating it into existing risk practices.

Part of the challenge is that climate scenario analysis requires a strategic and long-term perspective that may not align with the short-term and profit-oriented goals of trading organisations. Furthermore, traditional scenarios do not have the level of granularity, which is required to be relevant, consistent, comparable, and transparent in a commodities trading context, considering the specific characteristics, drivers, and uncertainties of the market.

To tackle these challenges, traders must expand existing scenarios, considering specific characteristics, drivers, and uncertainties, and use them to further stress test their portfolio against specific risks, rather than their overall strategy or business model.

For example, scenario analysis can be used in conjunction with traditional methods such as VaR to enhance market risk management. While traders will continue to use VaR to measure the baseline market risk of their portfolio based on historical data and a given confidence level, scenario analysis can be used to test how their portfolio would perform under various climate scenarios that may deviate from the historical data or assumptions.

Another good example is credit risk. Climate change can significantly increase the risk of counterparts defaulting on their obligations, through physical damage to their assets and operations, or increased exposure to regulatory and legal risks. Traders should look to incorporate climate risk metrics into existing credit risk tools and processes, such as internal credit ratings. This is particularly relevant where traders may have longer-term exposure to counterparts, such as in markets like LNG where long-term contracts are common.

Observation 5: Climate reporting is aligning with financial reporting.

Climate reporting is no longer a distant task owned by a sustainability function. Under pressure from banks and regulators, traders are increasingly aligning their climate reporting to their financial reporting, with ownership coming under the CFO.

This will be further reinforced with the uptake of ISSB. The IFRS S1 and S2 standards build on existing frameworks such as TCFD but are directly aligned to existing financial reporting standards, using the IFRS language to connect sustainability reporting to the balance sheet. Climate reporting will be required at the same time and for the same period as financial statements, and it is integral that finance departments play a material role in managing the disclosures.

Alignment with financial reporting will also help link climate-disclosures to the business and drive change. For example, ISSB requires climate risks to be integrated into financial planning and decision-making. This will enable traders to better quantify the implications of climate change on their financial indicators, position, and prospects, and to disclose how they are managing and mitigating those risks.

Ultimately, alignment with financial reporting will enhance the credibility and comparability of climate disclosures, as they will be subject to the same level of assurance and governance as financial statements.

Commodity and energy traders should be proactive in developing and implementing robust climate-related disclosure policies and practices that meet the expectations of their stakeholders, including banks. This will not only help them to comply with the regulatory requirements, but also to enhance their reputation, competitiveness, and resilience in the face of climate change.

Baringa can help trading companies navigate the challenges and opportunities of climate reporting, leveraging our deep expertise in commodity and energy markets, risk management, data analytics, and climate regulatory reporting.

To learn more about how Baringa can support your climate disclosures, please get in touch with our authors, Christian Linsday, India Hicks, Tibor Horvath and

David Kane.

Our Experts

Related Insights

Demand-led SMRs: A 'government-last' model to power industrial growth through privately funded SMRs

Drawing on engagement with over 100 potential investors and deep analysis of UK energy market structures, this report sets out a 'Government-last' approach to SMR deployment.

Read more

Simplification, not suspension: why CS3D still matters for executive teams

CS3D timelines have shifted, but the cost, risk and opportunity remain. Learn why executive teams should act now to manage supply‑chain risk and value.

Read more

Carbon capture heats up in Asia: Will it cool down the planet?

Carbon capture’s rising role in Asia’s energy transition

Read more

From ambition to action: making the most of the Warm Homes Plan

An expert roundtable discussion on the UK Warm Homes Plan, exploring how government, local authorities and industry can deliver home energy retrofits at scale, reduce fuel poverty and accelerate low‑carbon housing.

Read moreRelated Client Stories

National Grid Transmission: Using AI to see risk before it happens

AI-driven FRAME project helps National Grid pinpoint asset risks, combining data and engineering insight to boost resilience and smarter decisions.

Read more

Driving clean energy momentum with Octopus Australia

How do you bring a complex hybrid project to financial close?

Read more

Advancing Australia’s clean-energy future with Edify Energy

How do you secure the balance-sheet strength required to scale and speed up green project development?

Read more

Global energy business: taking control of IT supplier spend to deliver sustainable savings

How a global energy leader optimized IT supplier spend to save $100M+ annually through a unified SaaS and software procurement strategy.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?