Defining good Consumer Duty outcomes

30 May 2022

The Consumer Duty requires more than a traditional implementation approach. If you can resist the temptation to go straight to a gap analysis and instead answer the hardest question of what good looks like, you will open yourself up to unlock huge potential.

Without defining what good outcomes are and how to measure them, you will struggle to make meaningful progress and risk failing to meet the Consumer Duty requirements.

The Consumer Duty is a chance to realign your corporate strategy and forge a closer link between your strategic objectives and operational measures on consumer outcomes. This would allow you to embed the ‘good’ customer outcomes that form the essence of the regulation into the heart of your organisation.

We set out how an alternative approach could help your organisation to capitalise on the opportunities of the Consumer Duty.

Link your Consumer Duty outcomes with your strategic vision

As each new ruleset comes into play, the conventional response from financial services organisations is to iterate and enhance their existing conduct frameworks. The prevailing culture is to dive straight into operations and look at how to meet the requirements piecemeal. While this approach has merits, a more effective approach would be to take a step back and reflect on the full implications across the entire firm. Thinking about the overall organisation, you could create the vision and strategic goals, before then looking at the various functions that contribute to the different aspects of customer outcomes from the top down. Drawing up your implementation plans for the Consumer Duty in this way might look and feel very different, but could drive cost efficiencies and benefits that go beyond just regulatory compliance.

Financial services organisations are rightly asking what ‘good’ looks like. In typical FCA fashion, the Consumer Duty has left a lot of uncertainty around what exactly is necessary. We know the answer isn’t going to be a list of prescribed and standardised customer outcomes, but should be viewed with a strategic purpose. It is the chance to bridge the gap between your commercial and customer strategies, as part of your broader strategic vision.

Build your outcome framework foundation

With our alternative approach, we recommend building an outcome framework around the four specific areas of the FCA rules: communications, products and services, customer service, and price and value. From your understanding and analysis of these rules, alongside your specific operational requirements, you can begin to define and map good outcomes.

With the base of your outcome framework in place, you can define your ambitions and delivery targets up front. From there it will be wise to identify the processes and controls in place already, which will inform the enhancements needed to deliver against your ambitions and targets. Using this method gives you a way to tie back your corporate strategic objectives to the specific measures required by the Consumer Duty.

Looking right through the customer journey

It’s important to bear in mind that the FCA’s requirements aim to address everything that happens along the customer journey, including any outsourced services, such as call centres. It’s therefore necessary to carry out a customer journey analysis. This includes assessing the key points along the customer journey where you can in any way influence the outcome for that consumer. It’s these key ‘moments of truth’ where outcomes become tangible for the consumer. This is also an opportunity for you to judge what the right outcome should be from a customer perspective and how to achieve these.

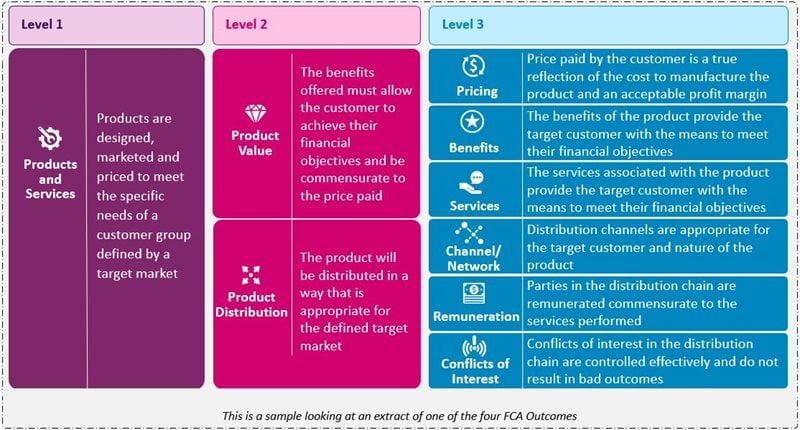

An easy way to think about this, is like a risk taxonomy, where you define your desired outcomes at a high level, then look at what is needed to achieve these outcomes at a more granular level. The process would include establishing your outcome statements (see figure 1) at level 1 and then breaking them down through level 2, 3 and beyond, until such a point where you’re satisfied you have measurable, but not too onerous, outcome statements. This would in turn identify and clarify what measures are needed to deliver these outcome statements, defining a tangible measure of what should be accomplished at all ‘moments of truth’ in the customer journey.

Figure 1: Illustrative example of an Outcome Taxonomy.

To be viewed in totality rather than each statement in isolation. The lowest level should be measurable and map back to the highest level that is comparable to the FCA outcome statements.

Realise the broader benefits, beyond just compliance

Working out what you’re trying to achieve rather than rushing into operational change creates an opportunity to enhance your organisation’s operating model, measure and report on desired outcomes, and establish a way to provide clear evidence to demonstrate your customer-centric culture. How can you make the most of the potential? Three priorities stand out:

Aggregate and report on customer outcomes to the board, regulators, shareholders and customers

With multiple overlapping regulatory obligations, you risk creating a "cottage industry" as you try to establish your key customer outcome data points. By reframing what you want to achieve and how you’re defining success, you can judge how to roll up your data to a level where the Board is able to debate and make informed decisions.

With your high-level outcome statements in place, it will be easier to understand the data required to share transparent insight. This in turn will empower you to report on Consumer Duty objectives not only to your Board but also to external parties such as regulators or shareholders.

Design and implement an enhanced operating model

A gap analysis or a maturity assessment is often the most conventional and straightforward route to compliance. While this is a useful exercise, these are typically managed in silos. Collective responsibility, on the other hand, present a greater chance to more effectively embed the regulations into your organisation by ensuring all departments are involved from the start, with an understanding of what is expected. This helps to prevent a siloed approach.

You can use an outcome taxonomy, for example, to give all areas of your organisation a true and comprehensive view of customer outcomes. Teams can use this to form a greater understanding of their processes and controls, linking these back to the key outcomes. This level of visibility will facilitate a clearer picture of how to deliver against these outcomes, and which people will need to be involved.

Understand what you really mean by a customer-centric culture

Most financial services organisations already claim to have a customer-centric culture, and many do. What is less prevalent are the measures in place to truly drive and provide evidence of this culture. There may be performance measures in pockets, but few will do this consistently across all four of the Consumer Duty outcome areas. This legislation provides a chance to articulate and assess what you really mean by your culture and values. You will need to be able to identify how and where your culture helps deliver good outcomes for your consumers. Additional benefits include being able to show customers what you’re tracking and measuring to report back to them on an annual basis. More and more, customers are looking for ethical firms and want evidence that firms are doing all the things they say they are doing. Now is the time to show how your strategy flows through to good outcomes for all consumers, to establish trust in the market and drive increased customer retention rates.

Are you ready for the Consumer Duty?

With full implementation of the Consumer Duty to be completed by April 2023 and the FCA wanting to see progress ahead of the deadline, preparations should already be well underway. We can help you design and implement a strategic outcome framework to tackle existing and future challenges and capitalise on the required enhancements, that not only meet obligations but build on your companies’ mission and strategy.

Alongside the information needed within your own business, the FCA wants to be more assertive in its supervisory approach, moving to a data-led culture, which is closely aligned with evidencing and reporting on good outcomes. Our next article will bring to light the importance of data within this changing regulatory environment: How much data is enough? And how should it be used?

If you'd like to know more about the incoming Consumer Duty and how you can enhance your strategy for good outcomes, please contact us.

Our Experts

Related Insights

Consumer Duty: What’s next? Five focus areas for the months ahead

The FCA’s Consumer Duty rules went live on 31 July 2023. We look at five key points firms should consider in the next 12 months.

Read more

Why the Consumer Duty will empower firms to combat greenwashing

What are the regulator’s intended outcomes from SDR and how are they linked to the Consumer Duty?

Read more

Essentials for Consumer Duty implementation

Struggling with Consumer Duty requirements? Meet FCA standards for better consumer care with Baringa's expert guidance.

Read more

Turning compliance into competitive advantage: how to move up the Consumer Duty maturity curve

Discover how to transform the Consumer Duty into a market differentiator. Explore maturity stages, benefits, and steps for maximizing your business potential today.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?