Partnership as the new leadership: Why collaboration is key to “greening” aviation

5 October 2023

Discussions about sustainability, climate change, and environmental, social and governance (ESG) frequently lead to the same conclusion – the need for collective action. Indeed, partnership as the new leadership was a recurring theme at Davos this year.

In the first article, we outlined the challenge facing the aviation sector. In this article, we will explore the role of the supply chain and encourage the industry to accelerate the transition to sustainable aviation.

Reassuringly, the technology required to produce and use SAFs is available. We’ve seen Sustainable Aviation Fuel (SAF) blended with traditional jet fuel and trialled in existing aircrafts without the need to redesign the fleet fuselage or engine design. Despite this trial reducing emissions by up to 70-80%, overall uptake remains low.

To scale SAF infrastructure and usage, investment and collaboration across the Value Chain is required – from the oil & gas majors producing and the airlines buying the fuel, to the airports, regulators and investors impacting the industry landscape.

Breaking the deadlock between supply and demand

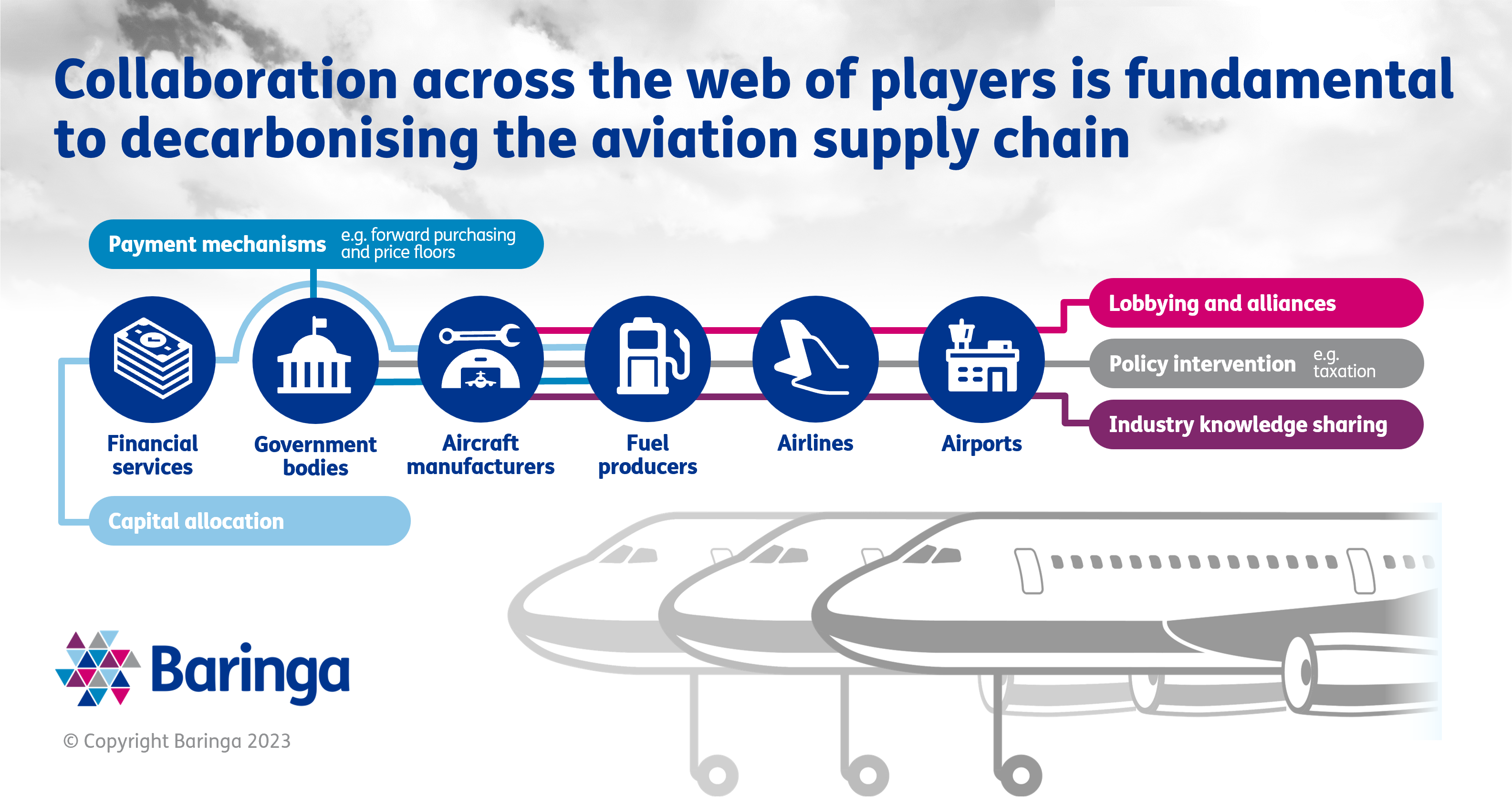

To understand why SAFs have not taken off yet, we need to assess the cards held by players across the aviation value chain. The value chain is a complex web of stakeholders, ranging from government bodies and financial services, to airlines, airports, fuel producers and aircraft manufacturers. Each player is at a different stage in their journey to Net Zero. Yet, where SAFs are concerned, they are collectively at an impasse.

On the supply side, the uncertainty of revenue and high upfront capital costs associated with SAF development is a barrier to scaling production. Ambiguity around topics, such as the true sustainability of feedstocks, creates uncertainty for investors considering capital allocation decisions in sustainable business, in turn avoiding the risk of stranded assets. Consequently, current levels of capital allocation into SAF projects is insufficient. This means that, whilst the SAF demand amongst airlines exists, the associated costs are still too high to secure predictable forward contracts.

As the urgency of the situation increases, so too does the need for infrastructure.

Without action and cross-industry collaboration, accountability will fall short between the ‘do-ers’ and the ‘enablers’, preventing the industry from achieving net zero.

Finding a fix: It is time for policy intervention

Policy intervention could be the catalyst to drive investors’ confidence in funding large-scale SAF projects. For example, upfront payments, forward purchasing and price floors would enable supply-side companies to increase production with guarantee of return on investment.

This policy intervention could drive increased demand for SAFs. With airlines operating on wafer thin margins, and the whole-life cost of SAFs being higher than that of traditional jet fuel, the option to pay a SAF premium poses a risk of revenue loss if not adopted by airlines globally. However, through levying additional taxes on the more polluting traditional fuel, governments could mitigate this threat to profit levels and the loss of competitive advantage by raising flight ticket prices at an industry-level.

For this to be effective, it is crucial that policy interventions are coordinated at an international level as SAFs would need to be available in both the departure and destination countries.

If successfully implemented, such measures would dismantle the barriers preventing widespread adoption of SAFs amongst airlines. This demand would drive financial institutions to invest in projects, accelerating the provision of high yield, low-cost SAFs.

Everyone has a part to play

Partnerships hold the key to this success. Stakeholder collaboration is crucial to boost both production and uptake of SAFs. Increased and faster adoption will be driven by policy intervention, and ensuring capital is accessible and affordable through financial incentives and fixtures. Economies of scale will drive down the overall cost of SAFs, while government-backed financial initiatives such as upfront payments, forward purchasing and price floors would give fuel manufacturers the confidence to increase production.

Throughout this shift, the sharing of knowledge, both within and cross-industry is not to be underestimated. Communication across the aviation value chain through alliances and peer events will raise the voice of the industry in lobbying for policy intervention.

Most importantly, everyone must act. From relatively small steps, like establishing or joining an alliance, to large-scale movements such as upfront payments, forward purchasing and price floors would enable supply-side companies to increase production with guarantee of return on investment. To achieve meaningful progress in cutting emissions and slowing down climate change, partnerships must become the new leadership.

To learn more about our work driving decarbonisation in the aviation industry, please get in touch with Megan Toon, Kristin Allan or Isabella Shortman.

Our Experts

Related Insights

Your people are key to unlocking the backlog burden

Crisis response is core to government, but agility alone is not enough. We explore how tackling root causes can prevent issues recurring and worsening backlogs.

Read more

Driving the digital shift in health: what to watch in the 10-year health plan

The 10‑Year Health Plan shifts from analogue to digital, putting power in patients’ hands and enabling the Neighbourhood Health Service and frontline delivery.

Read more

UK Spending review 2025 – impact and challenges for the public sector

Explore the 2025 UK Spending Review’s impact on public services, tech investment, and the challenges facing government departments.

Read more

Restructuring the UK Government: Risk, Reckoning, or Renewal?

Read moreRelated Client Stories

Delivering millions in productivity gains through AI adoption

Our client, a central government department, faced challenges in adopting AI into its operations. While there were pockets of experimentation, there wasn’t a clear understanding of how to scale AI across the organisation.

Read more

Working with a Government department to achieve a green NISTA review

Delivering pace and clarity in a complex government transformation involving multiple partners and shifting priorities.

Read more

Enabling a more efficient and sustainable future for a major state prosecution service

What does it take to ease pressure on solicitors and run a more efficient, sustainable prosecution service?

Read more

Delivering an independent evaluation for the NSW Advocate for Children and Young People

An independent evaluation of the NSW Strategic Plan for Children and Young People 2022–2024 was conducted to assess its impact and support future planning.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?