If flying doesn’t get cleaner, the UK may have to cut more than half its flights to meet net zero

20 June 2023

Aviation is one of the hardest sectors to decarbonise: demand for flying is growing, and there are very few easy ways to reduce emissions. If aviation doesn’t reduce emissions, the sector will not meet its decarbonisation targets and pressure to curtail demand will increase.

We believe the Department for Transport (DfT) needs to do two things:

- Sustainable Aviation Fuel (SAF) - Provide a clearer plan, followed with a stronger policy framework, to reach the 10% SAF target by 2030. DfT is currently consulting on this topic. The work plan that follows from this needs to outline multiple different scenarios, and directly confront the system-wide trade-offs that currently exist (particularly around availability of different feedstocks.) Look out for the second article in this series, where we will focus directly on the barriers to scaling production, and what should be done.

- Demand management - start to develop a contingency plan outlining key milestones to reduce aviation emissions and outline how demand management could work if sufficient progress isn’t made.

The aviation industry has bounced back. Aviation was crippled by Covid and in the immediate aftermath recovery was slow. However, two years on, leisure flights have rebounded to near pre-pandemic levels. The main reasons for this are a strong rebound in demand (pent up during Covid), China lifting its travel restrictions earlier this year, and oil price inflation being lower than expected.[2]

Emissions are climbing again, and will keep climbing

Flying more means more emissions. However, it’s easy to underestimate how intensive flying is, aviation is a sizeable share of the UK’s emissions – contributing about 8% of total emissions. If you regularly eat meat, you could go vegetarian all year, only to undo all your hard work with a return trip from London to New York at Christmas.

The rebound from Covid demonstrates that people want to fly. Business trips are increasingly replaceable with virtual meetings. However, not all experiences are as easily accessible without flying.

The global demand for flying is expected to grow – with some forecasts seeing flights in 2050 to be double 2019 levels. This increasing demand means that the share of aviation in both UK and global emissions is likely to grow. Additionally, non-CO2 emissions from contrails cirrus and nitrous oxides make aviation’s total climate impact two to four times worse than the impact of CO2 alone, according to the European Union Aviation Safety Agency (EASA).

Decarbonising aviation is hard

UK emissions are about half where they were 30 years ago, with some sectors decarbonising much faster than others.[3] For example, emissions from the power sector in the UK have fallen by two thirds (less coal, more renewables.) This is despite the size of the economy increasing more than two and a half times. Over the same period, however, UK aviation emissions have more than doubled.

A sector can decarbonise through two avenues:

- Do the activity less (eat less meat, reduce your thermostat, take less flights)

- Reduce the carbon intensity of the activity e.g. drive electric vehicles over petrol and diesel cars, produce power from renewables instead of coal, heat your house with a heat pump instead of a gas boiler, fuelling aircrafts with sustainable aviation fuels).

On both these avenues, aviation has and will continue to struggle. People want to fly and will continue to want to fly. Further reducing the amount of carbon emitted from each flight is extremely challenging.

The main avenue for decarbonising now is sustainable aviation fuels. Over the next decade, SAFs are the primary lever for decarbonising in Government's High Ambition Scenario.[4] Ready now, these are ‘drop in’ fuels, and can be blended with jet fuel today without modification to existing aircraft (or significant changes to refuelling infrastructure, like will be required for electric or hydrogen planes). The UK set a target to mandate that 10% of jet fuel used in planes by 2030 is SAF. The production challenges associated with generating enough SAF to meet this target are significant.

While SAFs play a significant role in carbon reduction, it is crucial to complement and strengthen these efforts with other approaches that contribute to overall emission reduction. These include:

- innovative aircraft design (incorporating aerodynamic improvements, lightweight materials, and efficient engine configurations)

- advancements in propulsion systems to enhance fuel efficiency

- the implementation of an improved air traffic management system through route optimisation and advanced navigation technologies

- improving ground operations, such as reducing taxi times.

If aviation can’t decarbonise soon, pressure to curtail flights will increase

Over the last few years, France have pushed to ban internal flights where there is an alternative train journey that takes less than 2.5 hours – a move that was approved by the EU Commission in December last year. In February this year, the Dutch government proposed a cap of 440,000 flights (with a cap of 460,000 being implemented) down from 500,000 flights per year to and from Amsterdam’s Schiphol Airport. There have already been calls to ban domestic flights in the UK, and with emissions unlikely to be cut drastically in the near term, these pressures will persist. This would mean the super wealthy (including Premier League Football clubs), would be forced to find alternative forms of transport for domestic trips. However, the bulk of the emissions lie in medium-long haul flights.

‘Demand management’ measures, designed to reduce the amount of flying can come in different forms. The strongest of these is bans on flights where there are feasible alternatives (like France’s) or caps on the number of flights allowed at airports (like Amsterdam’s). Softer measures include a frequent flyer tax (proposed by the Climate Change Committee (CCC) for the UK), levies targeted at premium (first and business class) flights (like those included in the International Energy Agency’s (IEA) Net Zero Scenario), or even a tax on jet fuel as seen in California. There are also behavioural (non-financial) interventions such as improving consumer information about the CO2 impact of flight and marketing of domestic tourism.

Unsurprisingly, policies designed to reduce the volume of flying (‘demand management’ measures) are unpopular with several groups. However, there is growing support for demand management from some groups e.g. the anti-flying movement Flygskam, a Swedish word which means flight shame. The popularity and fairness of any policy is likely to depend upon the specific design and which groups are affected. Untargeted taxes on flying disproportionately affect the disposable income of lower-income households that fly, while policies targeted at frequent fliers or those in first and business tend to affect wealthier households.

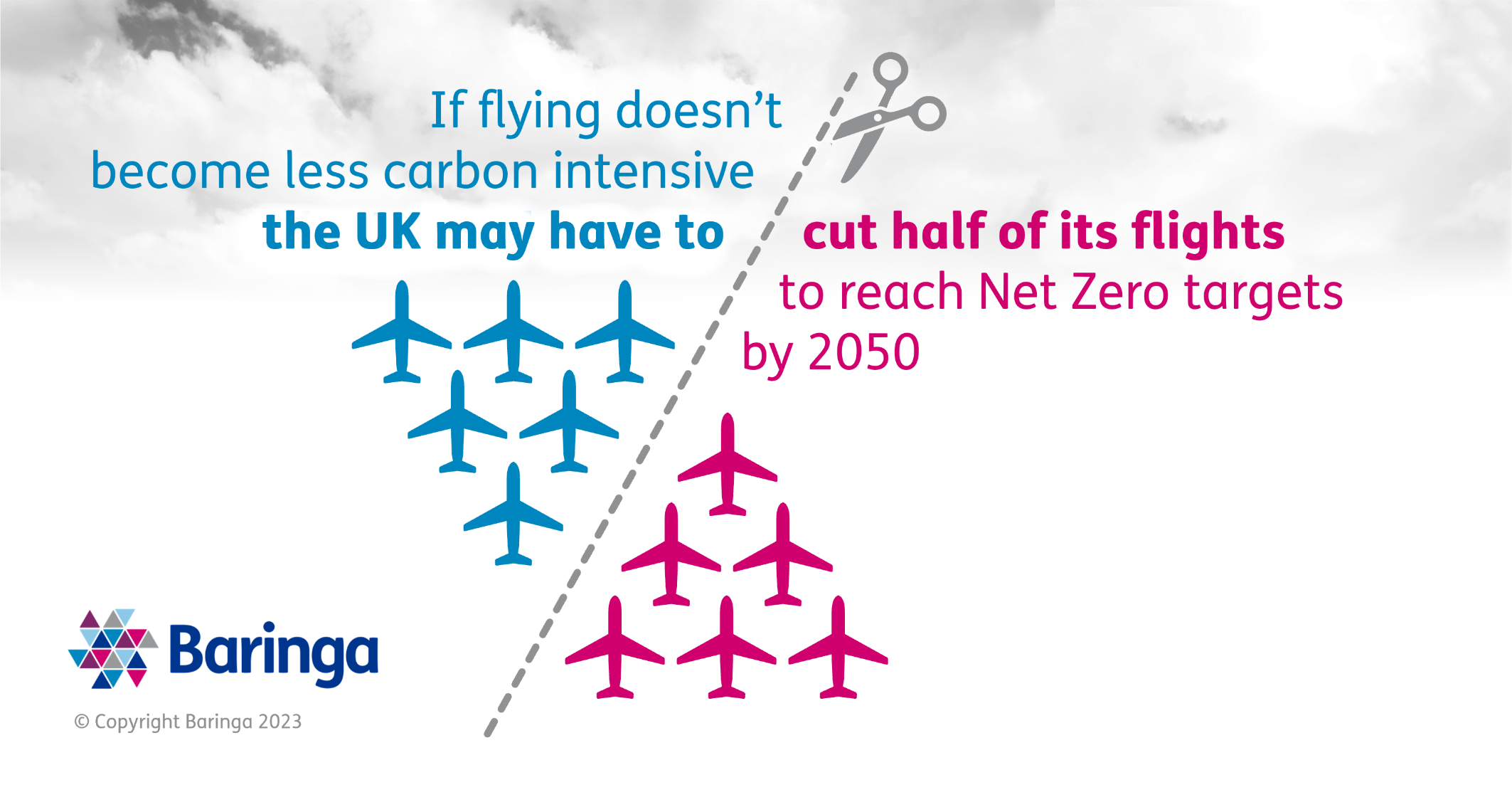

The UK Government’s Jet Zero Strategy steers clear of demand management measures, suggesting aviation can reach net zero without having to reduce demand.[5] However, the CCC’s Net Zero Scenario sees demand management measures playing a critical role. In a ‘Business as Usual’ scenario, the CCC project the sector to emit more than 50 Mega Tonne of Carbon dioxide equivalent by 2050, a 25% uplift on pre-Covid levels. In their Net Zero consistent scenario, the CCC only ask the aviation sector to meet a little over 20 MtCO2e by 2050, with the rest being picked up by out of sector offsets (such as greenhouse case removals).

That means that in the absence of any improvement in the carbon intensity of flights (above the 0.7% improvement modelled in the baseline), for aviation to meet its sector effort share, the UK could be looking at having to reduce one in two flights.[6]

We believe that the DfT needs to start creating and socialising a contingency plan. Outline the progress that needs to be made to reduce absolute emissions from the sector and by when. It should work through options for how, if low emission technologies and solutions are not available in time to meet targets, demand, including airport expansion could be managed to enable the aviation sector to meet its effort share. There are a series of complex trade-offs that need to be worked through, doing these earlier and having a plan prepared will minimise disruption years ahead.

This must be done in a way that:

- minimises impact on low-income earners

- incentives airlines to decarbonise

- minimises negative economic consequences.

In the second article of this series, we’ll be exploring the first of these supply-side measures, the difficulties the aviation sector has faced in securing a decarbonised value chain and our thoughts about how to over-come these challenges.

Whether you are in industry, government, a passenger or just interested in this topic and would like to learn more about our work driving decarbonisation in the aviation industry, please get in touch with Aaron Goater, Nikhita Swarnkar or Amy Breckell.

[1] ~40 MtCO2e in 2019 (7%), ~50MtCO2e if no additional decarbonisation beyond fuel efficiency improvements assumed in the baseline, ~23MtCO2e to be on the CCC balanced net zero pathway] (50-23)/50 is a greater than 50% drop i.e. in order to halve emissions to be on track for NZE, flights would need to halve in quantity

[2] Post Covid demand has also seen particularly strong demand for ‘luxury’ leisure travel (business and first class) People Are Splurging on Business and First Class Seats Post-Pandemic (businessinsider.com)

[3] https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/957887/2019_Final_greenhouse_gas_emissions_statistical_release.pdf ‘emissions’ here is referred to in absolute terms (not intensity) pg 15

[4] Jet Zero Strategy. We also refer to emissions here as absolute emissions

[5] jet-zero-strategy.pdf (publishing.service.gov.uk) pg 10

[6] If aviation doesn’t meet its sector effort share, then emissions will need to be reduced in other sectors (eating less red meat, driving less, more greenhouse gas removals)

Related Client Stories

Improving data preparation and collection for better State Government decisions

How do you collect and translate inconsistent data from disparate systems to better inform and evaluate the impact of spend policies?

Read more

Putting a social outcomes lens over an IT RFP for an Australian government agency

How do you change how vendors see their systems, so responses align with agency outcomes and non-functional requirements?

Read more

Ensuring climate compliance and lasting impact for government agencies

How do government agencies navigate climate regulations today and future-proof for tomorrow?

Read more

Delivering NHS England’s most complex non-clinical technology procurement ever

Supporting NHS England build the data backbone that will unlock better health services and care for people in England for years to come.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?