Europe’s gas consumers in the driving seat

How can gas/LNG buyers capture value and resilience in a fast-evolving LNG market?

5 min read 5 September 2025

From dependency to diversification: How European gas consumers are rebuilding gas supply

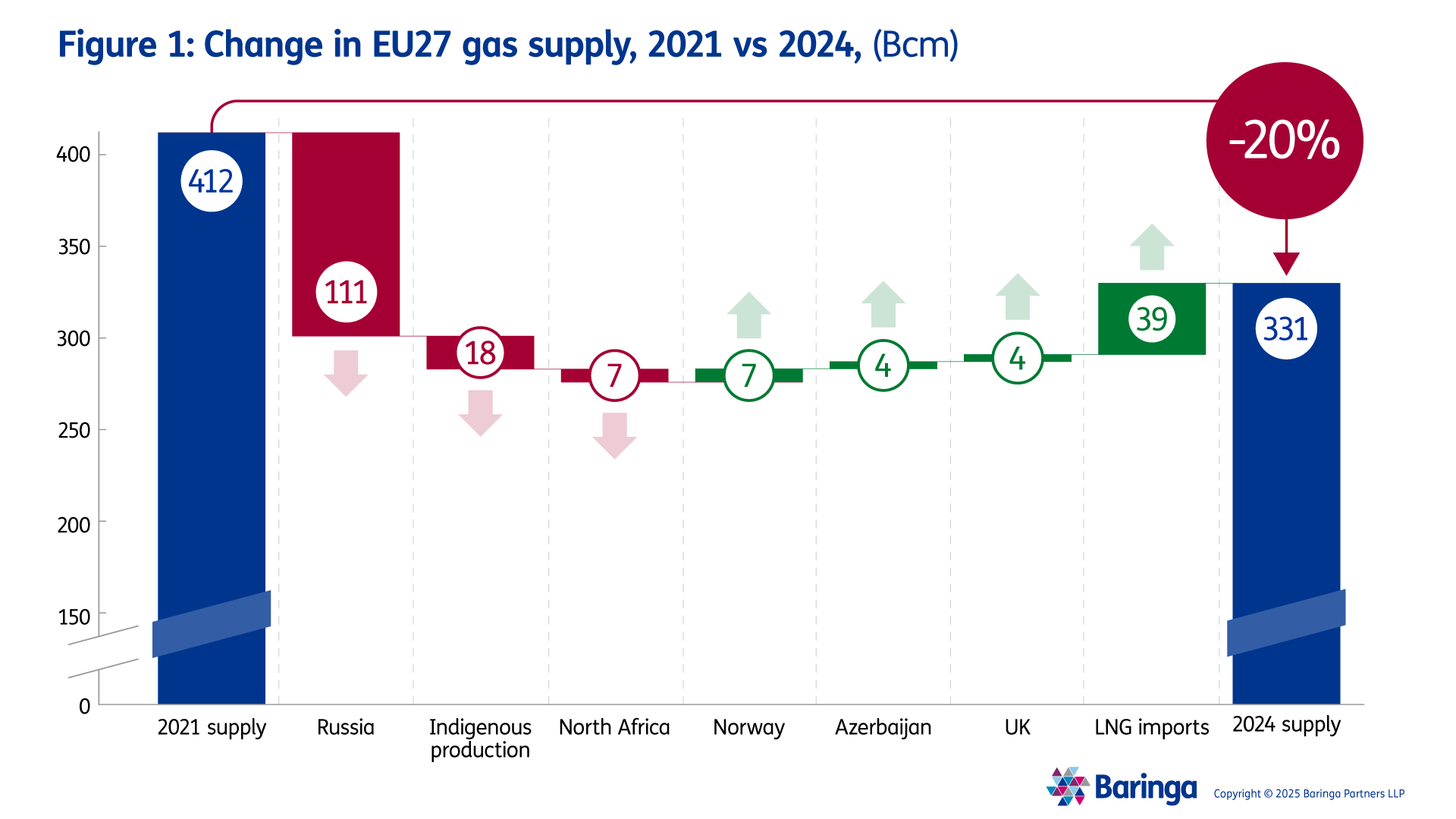

Over the last three years, the Russia-Ukraine conflict has drastically restructured European gas market fundamentals. The region has all but stopped its import of Russian pipeline natural gas, coming down from 144 Bcm in 2021 to 33 Bcm in 2024. That figure is set to drop further this year as Russian gas imports passing through Ukraine cease, following the expiration of a 5-year transit agreement. Out of the four pipelines that once flowed Russian gas to Europe, only the Turkstream remains operational to service what marginal flows remain.

LNG has filled the gap, with imports into Europe rising 46% between 2021 and 2024. Europe’s location between the US and Qatar, coupled with extensive regasification capacity and deep hubs such as TTF, cements Europe’s role as the premium landing point for global gas.

For European gas consumers, this shift presents not only challenges but also real opportunities to secure supply more flexibly, competitively, and strategically than ever before. This piece explores the key themes, opportunities and challenges that these changes present to large European gas consumers.

A number of key themes are reshaping the European gas and LNG markets

The European gas and LNG market is undergoing structural changes, creating new opportunities for major consumers to secure supply that is both flexible and affordable. Rising US LNG exports and the rapid build-out of European regasification capacity are transforming how gas is procured and traded. At the same time, shifts in Asian demand and a slower pace of decarbonisation are opening further avenues across the gas and LNG value chain. To capture these opportunities, European consumers must be proactive in making informed choices on contracting, infrastructure access, and partnerships to maximise value for their companies, shareholders, and customers.

Key Gas and LNG Themes and opportunities for European Gas Consumers

| Theme | Opportunity for large European gas consumers |

| Upcoming US supply |

|

| Market trading and optionality |

|

| EU LNG import capacity growth |

|

| Declining Asian demand |

|

| Slowing pace of decarbonisation |

|

The opportunities are not without complexity. The ability to capture value lies in using optionality in regas access, trading and in contracting structures, while navigating supply, policy and transition risks. At Baringa, we help large gas consumers turn this complexity into a competitive advantage.

Key challenges to consider

| Theme | Challenges to consider | How We Can Help |

| Upcoming US supply |

|

|

| Market trading and maturity |

|

|

| EU LNG import capacity growth |

|

|

| Declining Asian demand |

|

|

| Slowing pace of decarbonisation |

|

|

To find out more about how to stay ahead in the European gas & LNG market, get in touch with Mashal Jaffery or Peter Thompson.

Our Experts

Related Insights

Middle East crisis 2026: impact on global gas markets

Explore how the crisis is disrupting global gas markets. Baringa’s analysis covers LNG flows, price impacts and risk scenarios for organisations.

Read more

Navigating AI governance for energy companies: why a holistic enterprise model is key to compliance

Energy companies adopt AI to enable their strategy, explore Baringa’s recommendations for harnessing it effectively while ensuring compliance and managing risk.

Read more

Intelligent asset management for energy companies

What is intelligent asset management, and how does it enable organisations to improve performance, reduce risk and make smarter, insight‑driven decisions?

Read more

How can a digital supply chain drive resilience in the age of the digital energy transition?

Four key areas where digital technologies have the potential to transform supply chain performance, profitability and resilience through the energy transition.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?