The passive decarbonisation problem

Why you should care about direct renewable energy procurement past 2030

11 March 2026

Despite recent rhetoric that the energy transition is slowing its pace, 2025 saw investment in the energy transition reach $2.3 trillion globally, with $690 billion in renewable energy specifically. Grids are decarbonising.

In recent years, investment in and deployment of grid-connected renewables across Europe, has contributed to Net Zero targets for several countries. Some corporates see this as an opportunity to scale back their ambitions, taking the ‘Passive Participation Approach’, meaning they decarbonise their emissions as the grid decarbonises. Some have scaled back their green certificate purchasing, and many have reduced their cPPA purchasing as these contracts have become more expensive, instead relying on the standard grid mix for consumption and reporting. Where companies are buying PPAs, the preference has been for less expensive, operational PPAs, rather than those that bring additional renewable assets online.

It is a compelling argument: 'If the grid will be wholly renewable, why should I worry about long-term renewable power contracts, especially when this could come at a premium to my current procurement approach?'

However, this doesn’t take into account the value of a sophisticated renewable procurement strategy, which accounts for:

- Grid decarbonisation: As this slows, what is the risk to you?

- Price certainty: What is the cost of price uncertainty?

- Reporting risk: What is the risk of non-compliance?

- Reputational risk: What are the consequences of not acting?

1. Grid decarbonisation: As this slows, what is the risk to you?

Grid decarbonisation will likely come a lot later than many expect, or at least later than government targets. Under current circumstances, our power market modelling displayed in Chart 1 projects power sector decarbonisation in GB by 2047, 12 years behind the Labour Government’s current target. Spain and Denmark fail to meet Net Zero by 2060, as unabated thermal capacity remains operational through the period modelled. The Netherlands lags their 2035 Nero Power target by 21 years, Germany by 8 years, and France just makes their 2050 target. Despite enduring low grid carbon intensity due to strong hydro power, Norway only crosses the 0gCO2/kWh threshold with wider adoption of BECCS and CCS. In short, it will be some time before the passive participation strategy pays off.

Chart 1: Baringa grid decarbonisation projection (power sector carbon intensity, gCO2/kWh)

Source Baringa

Our projections consider multiple factors across government intervention, technology, carbon and commodity costs, demand growth and deployment of different technologies in renewable, low-carbon, thermal and storage. In general, we project that these markets fail to reach their Net Zero targets due to government intervention or market incentives being too weak, carbon prices too low, renewable deployment too slow and an enduring reliance on gas to provide firm capacity. While these trajectories are uncertain, government policy can act as the driving force to overcome these challenges, namely, the continuation of strong renewable policy and a popular consensus for pro-decarbonisation agendas in government.

Recent political unrest has emphasised a real risk of significant bumps in the road for many countries’ decarbonisation trajectories. In the US, Trump’s One Big Beautiful Bill Act has shifted support away from intermittent renewable deployment, towards dispatchable power, as the ‘energy emergency’ grows in political salience, and Security of Supply overtakes the decarbonisation agenda. The country has already seen the impact of the Bill, with Trump cancelling what was to be the US’s largest solar project, Esmeralda 7, forgoing up to 6.2GW of renewable energy.

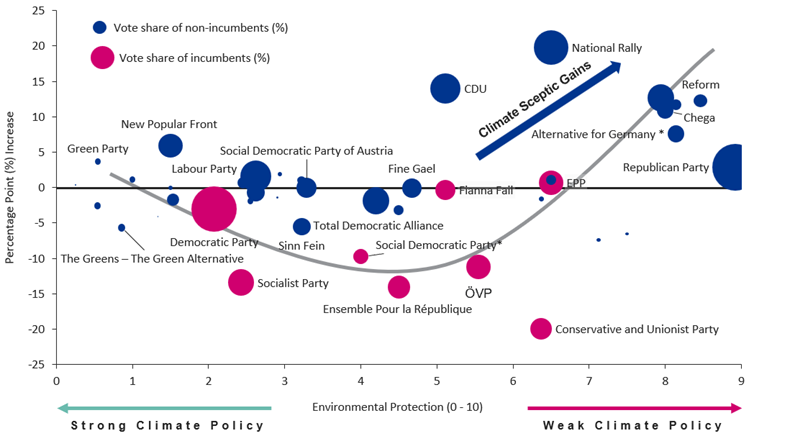

2024 was a year of worldwide elections, with half the world’s population having the opportunity to vote. Two clear shifts emerged. Firstly, incumbent parties performed poorly in most countries. Secondly, climate sceptics made gains in some regions, representing a less universal—but still important—challenge to the climate consensus. Chart 2 shows the recent swings favouring parties with weaker climate policy, and should act as a caution to more bullish renewable build-out projections.

Chart 2: Change in vote share 2024 (relative to the previous election result) by party climate policy

Source Baringa

The wavering political commitment to climate policies may result in grids not being decarbonised in line with current national ambitions, and therefore, corporates cannot rely on a steady downward trend in their Scope 2 emissions. While this may catalyse direct renewable contracting for some, others may swing in the opposite direction and start to question whether there is any merit in maintaining momentum and investments to meeting their carbon and wider ESG commitments.

This is a question we are helping energy and sustainability teams work through with their executives, especially in the light of changing reporting standards like the Greenhouse Gas Protocol and Science Based Targets Initiative. Why should I still care about this when we are behind schedule and it appears the climate agenda is waning at the national level? In our view, part of the answer concerns risk, namely, mitigating price, regulatory and reputational risk.

2. Price certainty: What is the cost of price uncertainty?

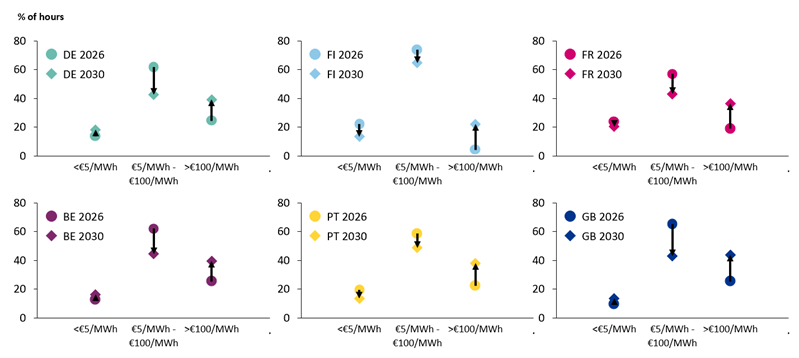

Enduring price volatility should motivate direct renewable procurement, with fixed-price contracts giving energy managers and CFOs certainty in the price they pay for their power. Even with increasing flexible technologies to dampen price swings, a low-wind, low-sun year could see power prices soar. Chart 3 displays how renewables drive hourly price divergence across different markets in the future. In all markets, the number of hours in the highest price range (above €100/MWh) increases.

Chart 3: Percentage of hours in different power price range (£/MWh)

Source: Baringa

Signing longer-term renewable energy contracts are a tool to reduce risk in a volatile market, providing a long-term hedge. On-site renewables have the added benefit of avoiding non-commodity costs, and corporates should therefore evaluate the cost of deploying behind-the-meter solutions against the potential savings to be realised by a lower overall power cost.

When signing cPPAs, corporates need to value the benefits of fixed price certainty against a potential increased 'all in' power cost, given the additional intermittency fees (i.e. firming, imbalance, etc.) that are applied on top of the Baseload power cost. The key here is understanding the trade-off between leaving yourself exposed to a volatile power market versus a potential premium to pay for price certainty with direct renewable procurement. Ultimately, this means corporates will need their own view of ‘fair value’ based on this trade-off.

3. Reporting risk: What is the risk of non-compliance?

The turbulent political support for renewable deployment may well be temporary. The bodies setting the standards for how corporates report emissions and set targets do not show the same wanning of requirements. As we discussed here, the Greenhouse Gas Protocol (GHGP) recently closed its Consultation on major proposed changes to reporting methods, which will likely bring in a new age of corporate renewable procurement. This is mirrored in updates to the Science Based Target’s Initiative (SBTi), which matches the GHGP’s move to hourly emissions reporting for the largest power users from 2030, with the share of reporting under hourly accounting increasing to 90% by 2040.

We recommend corporates ‘get ahead’ of these changes. Reduce the risk of non-compliance with these initiatives, and move quickly before the demand for direct renewable contracting swallows the pipeline of available projects. Some assets will no longer produce eligible Energy Attribute Certificates (EACs) to count towards Scope 2 decarbonisation under newly introduced asset-age criteria. This and hourly reporting will likely bring an end to the inexpensive EACs we have seen in recent years, and push corporates towards direct renewable procurement via additional PPAs and on-site renewables as the best option for adhering to new standards.

While additional PPAs will be one way to de-risk a future Scope 2 position for GHG Protocol and SBTi, they have, and likely will continue to trade at a premium. Corporates need to decide on their willingness to pay for a better demand match position, and consider how they can strengthen their demand match by building an optimal PPA portfolio to their demand profile, typically achieved through contracting a blend of renewable technologies, plus implementing storage technologies and demand flexibility.

4. Reputational risk: What are the consequences of not acting?

The final risk centres on the reputational and, in some cases, financial risk of failing to meet Scope 2 targets. Recent years have seen heightened scrutiny from investors, regulators, customers, employees, and wider society. Any retraction in ambition will not go unnoticed, inviting greenwashing critique, eroding trust in the brand and reducing investor confidence in the business strategy.

Websites like Net Zero Tracker, the SBTi’s own target dashboard, S&P Global’s Commitments Tracker and accreditation companies like EcoVadis have made it easier than ever to monitor companies’ commitments, progress and credibility across Sustainability topics. Complaints have been made to advertising regulators about misleading renewable energy claims, receiving media critique, such as those raised against Budweiser in 2024, TotalEnergies in 2025, and Renault, Virgin Atlantic and others. The reputational damage of watering-down and failing to meet renewable energy commitments should not be underestimated.

In essence, the ‘short-termism’ of current approaches that look to minimise cost and meet minimum standards and stakeholder expectations fails to prepare for the changing energy system and fails to value the benefit of acting early. Large energy users cannot rely on decarbonisation at the National scale; they have an active role to play in driving the transition, in turn reducing their exposure to price, regulatory and reputational risks.

Explore related content

Reporting scope 2 emissions: the GHGP's new consultation

The GHG Protocol is under fire for enabling questionable Scope 2 reduction claims. Read on to understand what the criticism means for your organisation.

Read more

Energy Source | Manage your power position

The only investment‑grade software designed to support your energy strategy, drive effective execution and strengthen your approach to risk management.

Read more

Mastering your renewable electricity procurement strategy

Watch our experts guide you through building and managing effective PPA portfolios, from strategy development to selecting tools for financial and commercial management.

Read more