Moving from intent to action: the inflection point for financial services in the climate transition

2 March 2023

Net zero targets are set. Strategies are in place. Now, to move from intent to action, banks must fundamentally transform, embedding climate into every aspect of business as usual.

The financial sector is leading the race to net zero – but time is running out

The world is at an inflection point. To have any chance at keeping global temperature rise under 1.5 degrees, greenhouse gas emissions must fall by 45% by 2030.

Banks, and the wider financial sector, have been setting the pace for this decarbonisation agenda. They’re fixing bold targets, signing up to collective commitments, launching programmes to meet emerging regulation and developing transition plans.

But now, banks need to move beyond target-setting and strategic planning to get to the core of the climate challenge – driving actual reduction of carbon emissions. It’s time to turn intent into action.

Everything to play for

Banks may be at the front of the pack in setting ambitious climate commitments, but few have the right operational set up to deliver them.

The challenge banks face is that climate still tends to be seen as an add-on to the business, instead of an integral part of business as usual. Some banks have central teams and committees for steering sustainability strategies and climate risk management. But these teams operate as specialised functions and remain siloed, leaving their efforts out of sync with everyday operations.

To deliver on climate commitments requires moving away from standalone teams and point solutions, and instead embedding the commitments as part of business as usual – a part of decision making, processes, governance, integrated reporting and embedded in functional capabilities.

Banks that get ahead of the curve now will reap the greatest rewards, including:

- Reduced programme delivery costs as processes become more efficient and standalone teams are consolidated into the wider business

- Greater commercial opportunities from emerging low carbon markets, bringing more insightful client conversations and longer term value for stakeholders

- A comprehensive transition plan with a traceable pathway for delivering against net zero targets and meeting regulatory requirements (we’ll explore this topic in more detail in an upcoming article dedicated to the Transition Plan Taskforce)

- Simplified governance that reduces risk management inconsistencies and leads to leaner and stronger controls

Rising to the challenge

With less than seven years to meet interim targets and 2030 goals, this is a pivotal decade for banks to accelerate their net zero efforts. As the window for change narrows, those that fail to act now will fall behind the curve – and jeopardise their license to operate in the eyes of regulators, customers and other stakeholders.

As conditions grow more urgent for banks to deliver their climate commitments, continued economic volatility is pushing them to cut costs. It’s a perfect storm of converging pressures:

- Increased regulatory pressure: Banks are having to adapt an increasing number of standards and regulations, such as UK listing rules, PRA Capital Framework reviews, and transition plan taskforce disclosures – to name a few.

- Pressure to drive sustainable finance growth: Banks are under pressure to accelerate their carbon reduction roadmaps and drive material sustainable finance growth in a highly competitive market

- Significant cost pressure: Finally, all the above – regulatory responses and decarbonisation plans need to be achieved at a lower programmatic and ongoing cost base

In the face of rising expectations at a time of cost constraints – how can banks do more, for less?

Integration as a catalyst for change

At Baringa, we believe that responding to these ongoing pressures and accelerating progress towards net zero targets requires banks to fully integrate climate – and more broadly, sustainability – into their operating models.

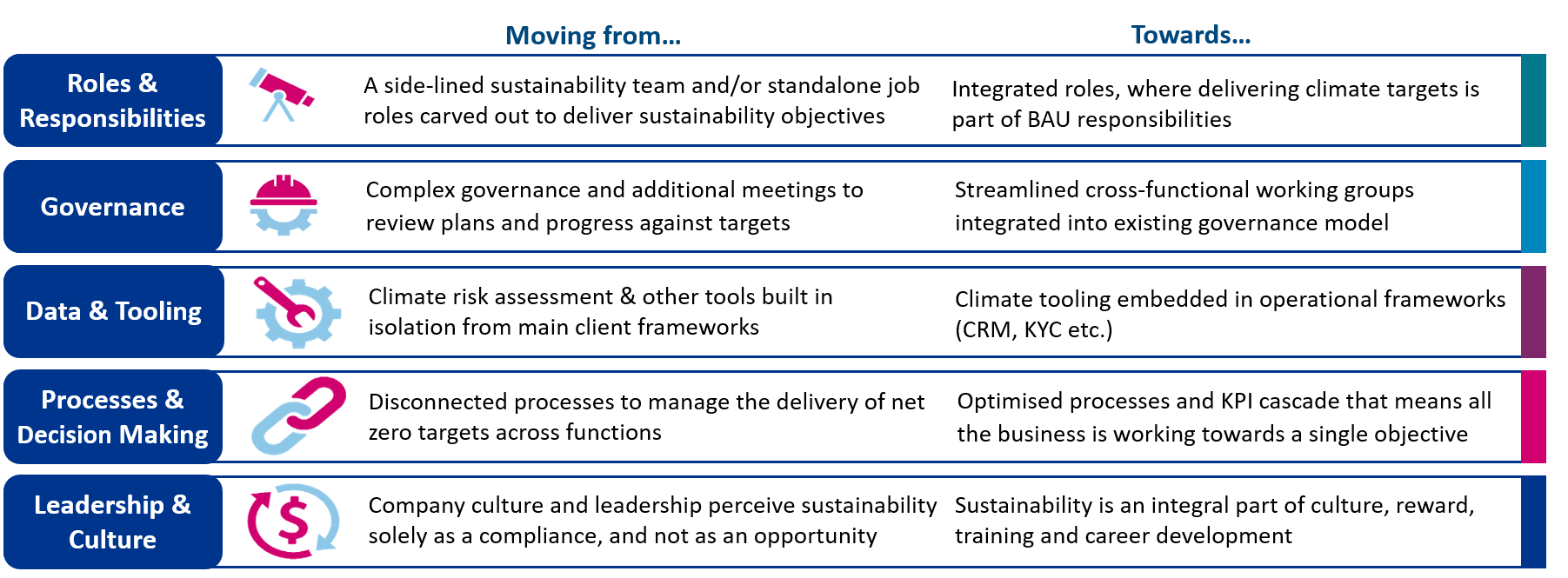

We don’t propose that banks create a completely new operating model (this would be complex, inefficient and unpractical). Rather, we believe integration is key. This includes expanding roles and responsibilities, and rethinking digital systems and performance metrics. In the image below, we’ve highlighted a few examples of how banks’ operating models need to change:

Some of our clients are already making this shift. For example, we have helped a number of global banks to remove standalone climate risk functions by building it into an existing risk management framework. We’re also supporting a European bank as it condenses its climate governance structure to embed climate related decisions into its governance model.

However, room for improvement remains. We see fewer banks fully integrating climate data into their BAU business processes and steering. An integrated climate data model is an essential component of consistent, meaningful reporting and risk assessment – allowing banks to better understand the risk and the commercial opportunities attached to their portfolios.

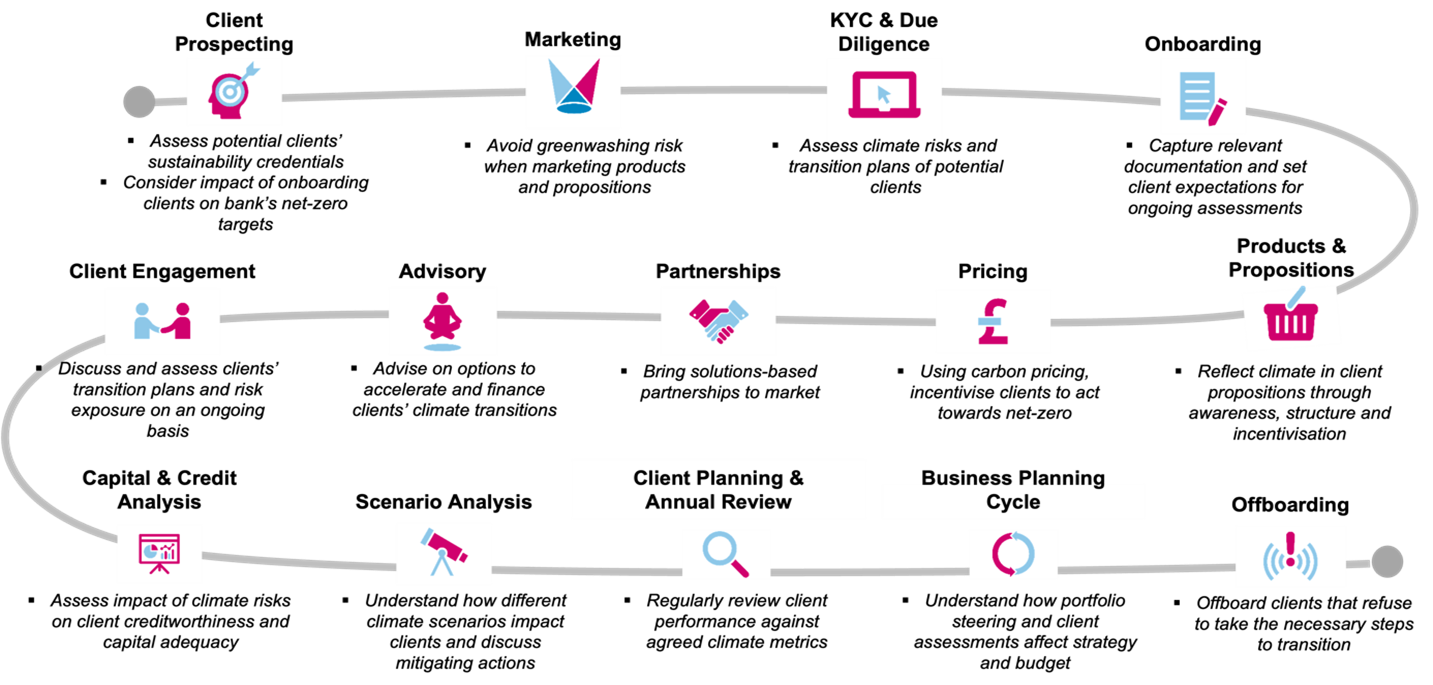

Rethinking roles and responsibilities across the client lifecycle

For banks to reinforce this evolved operating model and fully realise their net zero ambitions, climate will need to become a part of everyone’s business as usual – not just the charge of specialised teams. To bring this to life, we can look at how roles and responsibilities would change across a typical client lifecycle, as mapped out in the image below.

To equip teams working across the client lifecycle with the tools and knowledge to deliver these new roles and responsibilities, banks will need to review their processes, governance and people management – adapting and enhancing existing structures and adding new ones where needed.

Delivering best in class sustainable client engagement

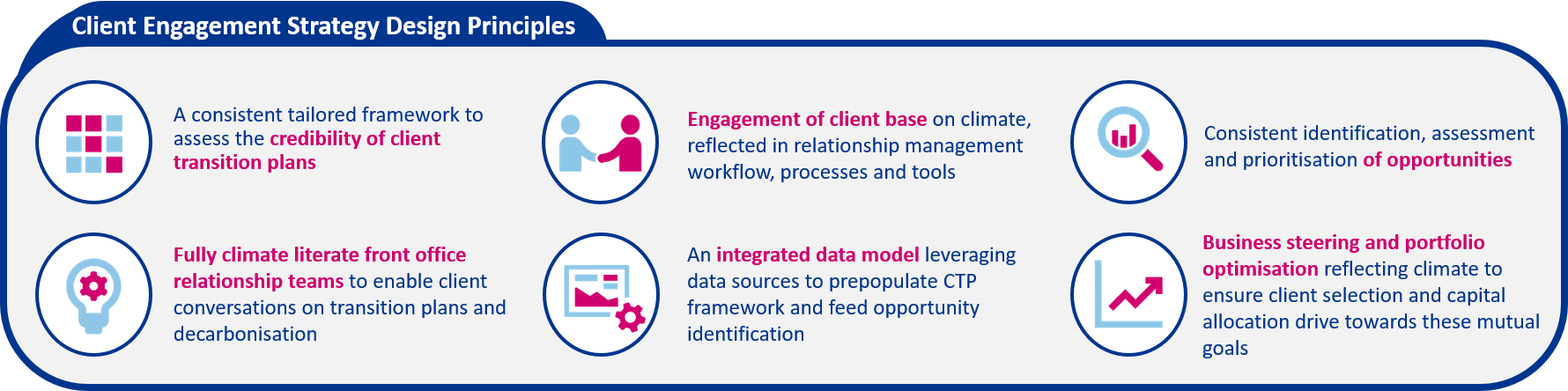

One step of the lifecycle receiving particular attention across the industry is client engagement. Typical responsibilities include driving conversations with clients, demonstrating the breadth of their knowledge, insight and sustainable finance solutions in a timely manner, while reacting to market triggers.

Ultimately, banks need to integrate transition plans and climate risk exposure into every client engagement. We believe success rests on incorporating six design principles, outlined in the diagram below.

While climate led engagement is a critical focus for 2023, and a key value driver, many banks are only just setting out on that journey. When we recently benchmarked a number of global banks in relation to their client engagement, we discovered that:

- All banks have an internal mechanism to assess their clients’ environmental performance, against specific restrictions. However, the assessment is often risk focused and the over three quarters either haven’t fully operationalised their credible transition plan assessment, or don’t yet use it to focus on transition finance opportunity identification.

- The majority of banks have upskilled their management and front office teams on climate broadly, and specifically climate risk. But more than 50% still need to introduce in depth, sector specific training programmes that will enable relationship managers to have meaningful conversations with clients.

- Most banks have a climate data capability, focused on financed emissions modelling and supported by external data providers. However, few have built a capability to identify and prioritise transition finance opportunities in high emitting sectors.

- Similarly, few banks have a systematic approach for engaging with clients on climate related topics, identifying and prioritising opportunities or business steering.

- Many of our banking clients remain focused on risks rather than opportunity. This is holding them back from exploring opportunities across their clients in all sectors and gaining a first mover advantage in bringing new climate finance offerings to market.

What’s needed for a successful transformation

In our experience, businesses on the front foot have systematically reviewed and reinforced their operating model to deliver their climate commitments. They’re leading the charge on turning intent into action:

- They embrace the processes and digital platforms that enable banks to obtain the data needed to measure and manage progress on their climate commitments, and to efficiently integrate climate into commercial activities

- They fully integrate climate KPIs and decision making into organisation wide roles and responsibilities

- They empower employees with climate training and performance aligned rewards, ensuring everyone is in pursuit of a single set of targets

- They take their client engagement strategy to the next level by using consistent frameworks and developing tools to become their clients’ transition finance partner of choice

Banks have played a pivotal role in building momentum for the net zero transition. Now, they must continue to lead by example – turning targets and transition plans into tangible action. By weaving climate into the fabric of their business and client engagement, banks can catalyse the change that’s needed to move their operations and the wider economy to net zero.

If you’d like to learn more about putting your climate strategy into action, stay tuned for more articles in this series. Next up, we’ll be taking a closer look at transition finance across key sectors. And in our final article, we’ll dive deeper into operationalising the journey to net zero in line with the Transition Plan Taskforce.

To find out how Baringa can help you transform your operating model and develop best-in-class client engagement to accelerate your net zero transition, please contact Tom Orr, Megan Toon and Polina Rozdestvenska.

Related Insights

Shaping Australia's superannuation future

Staying ahead in volatile markets. We help you navigate regulatory pressures and stakeholder expectations to drive better member outcomes and long-term value.

Read more

Navigating the path to sustainable reporting: insights from the IFRS Sustainability Symposium 2024

Baringa’s insights from the 2024 IFRS Sustainability Symposium, highlighting the key themes shaping the future of sustainability reporting and disclosure.

Read more

If ESG isn’t consistently understood, how do super CROs manage this risk?

Learn how superannuation funds and Chief Risk Officers are managing ESG-related risks in this evolving landscape.

Read more

How should super CROs respond to evolving climate change expectations?

Discover how superannuation funds adapt to evolving climate change expectations and the challenges faced by Chief Risk Officers.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?