Is Web 3 the future of payments?

20 October 2022

Web 3 represents the next iteration of the internet – it will be powered by distributed ledger technology (DLT), which is redefining how payments and the exchange of value is executed. DLT will make payments simple, data rich and efficient, removing the need for intermediaries. The world of payments has woken up to Web 3, with the biggest players in the industry now fighting for their place in the metaverse.

Web3: A timeline of payments

Why are payments and Web 3 interlinked?

Web 3, by design, is borderless, data rich, resilient and easy to reconcile – all attractive attributes for a payment ecosystem. So, the move from traditional payment rails to a DLT enabled environment is a logical one if the scalability challenges of supporting the volume of transactions required to support an efficient economy.

To bring this to life, in 2021, Visa announced their partnership with 50 cryptocurrency firms to enable customers to spend digital currencies at 70 million merchants worldwide. A strategic move like this, from a traditional payments company into the crypto space, highlights the significant shift in thinking and momentum Web 3 is gaining.

According to Brandessence Market Research, the Global Crypto Payment Gateway Market is expected to grow with the CAGR of 22.8% from 2022-2028. At Baringa, we’ve been looking at the impact DLT is already having in the finance sector. This presents countless opportunities in payments to build a more resilient, efficient, and reliable infrastructure. In particular, the rise in DLT utilisation will have a substantial effect on the payments experience for consumers and businesses around the world.

Why are payment systems so important to consumers?

We all rely on payments in exchange for goods and services. For a long time, the physical exchange of cash was the primary payment method -- however with advancements in technology, such as the internet, payments have become digital, enabling the smooth functioning of our global economy.

The digitisation of payments has shifted consumer behaviours: Card payments have progressively become the most popular payment method in many countries, in particular through contactless payments, whilst physical cash has slowly declined.

""In 2021, 14 million Britons had a digital only bank account and today, 93% of UK adults are using online digital banking services"

However, the technological advancements in payments have not been without drawbacks. Digital payment journeys involve many hidden intermediaries which lead to increased costs and slower processing. A prominent example of this being Amazon’s threat in 2021 to stop accepting Visa Credit transactions due to “continued high cost of payments”. This emphasises the demand for a shift to a more efficient and cost-effective way of making payments for both consumers and merchants – achievable through Web 3.

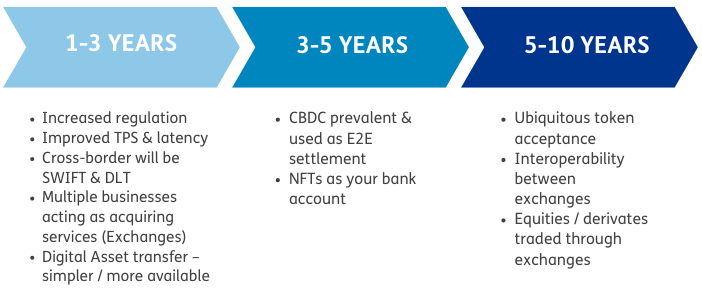

Our view on consumer trends in Web 3 over the next 10 years

Phase 1: One to three years

Financial services are one of the most regulated industries and post 9-11 attacks saw the strengthening of terrorist financing and Anti Money Laundering (AML) regulations. In 2014, BNP Paribas was fined $8.9bn for failing to comply with US AML regulations, when concealing transactions for countries actively sanctioned by the US.

However, current regulations do not transpose well into the digital asset ecosystems without significantly reducing the benefits digital assets offer consumers. An innovative approach to regulating the space will emerge, taking advantage of the benefits digital assets provide in terms of transparency. This will include leveraging artificial intelligence and machine learning to identify malicious or criminal behaviour, while enabling consumers to retain the benefits digital assets offer.

With the improved regulatory frameworks, traditional finance and the new digital asset ecosystems will see bridges built between them to allow value to flow seamlessly between the two systems, empowering enterprises to enhance their propositions. Key to this will be the need to regulate these digital assets at a global level, and not in geographical siloes requiring closer alignment of global regulatory bodies.

Alongside enhanced regulatory scrutiny, the underlying technology is set to rapidly advance with our predictions that over the next 3 years, Transactions Per Second processing (TPS) will increase to meet the current standards seen in traditional payment infrastructure.

Correspondent banking will be a mix of traditional clearing through SWIFT, with a growing volume through DLT enabled clearing platforms with multiple options for how you move your money in a borderless Web 3 world.

Digital assets will be transferrable at pace and used more ubiquitously as a store of value.

Phase 2: Three to five years

Whilst innovation continues with fungible and non-fungible tokens, we believe one of the most tangible areas of change for Web 3 payments in the next three to five years will be with CBDCs (Central Bank Digital Currencies). Although CBDCs are a concept that only became popular in the past 3 years, they’ve been around for some time with more than 100 countries currently exploring CBDCs China, for example, launched an initial study on digital fiat currencies back in 2014 and then piloted their digital Yuan in 2021, for public use. Now, other countries, like Australia, are beginning their own digital currency pilots. In the medium term, we can expect to see more pilots being launched, and in turn, a prevalence of CBDCs in end-to-end settlements. With this comes a host of economic benefits in payments – more safety, lower costs, greater financial inclusion, and a more efficient settlement process – especially for cross border payments.

In addition to CBDCs, our predictions for the Web3 ecosystem are linked to the widespread adoption of NFTs to assist interbank products. NFTs are programmable doorways to services which will shape future propositions and revenue generators, including NFTs replacement of existing bank accounts.

Phase 3: Five to ten years

With the increasing adoption of CBDCs globally, both in retail and corporate environments, we anticipate the focus will move onto providing and managing access to the evolving Web 3 world. Providing the ability for everyone to manage and seamlessly use their portfolio of digital assets will be key to driving adoption.

And those that can provide a streamlined and frictionless experience will be the front-runners. Decentralised exchanges need to be interoperable across preferred token types . Consumers will not need to off-ramp to legacy fiat currencies as digital currencies will be just as easy to transfer and accept as payment, and all within the control of their own digital wallet.

Our predictions for payments in a Web 3 ecosystem are underpinned by how distributed ledger technology will shape the next 10 years. In summary, it would be wise to watch out for increased regulation in the short-term, with CBDCs becoming more prevalent in the mid-term. Then it’s all about embedding and streamlining these processes to ensure enhanced customer experience across all Web 3 products.

DLT can be seen as a credible delivery engine to solve process inefficiencies and bottlenecks. However, we recognise that DLT will not be the answer for every use case with technology continuing to advance at an astonishing rate, as we’ve already seen in the past 10 years with the move away from cash towards digital payments.

To find out more about how we can help you on your Web 3 journey, please contact us.

Our Experts

Related Insights

The role of regulators in accelerating Web 3 innovation

Financial institutions are seeing the potential that Web 3 technologies can offer but need the regulatory guard rails to have the confidence to commit.

Read more

Solving the KYC dilemma with Web 3

DLT has great potential to optimise Know Your Customer. We unpack the issues in KYC for retail and corporate banks and evaluate the application of DLT.

Read more

Blockchain opportunities for treasury – disruptive solutions or additional risks?

We take a look at how Web 3 is impacting investment banks, specifically bond issuance, intraday liquidity and in OTC derivatives.

Read more

Why NFTs are here to stay

What is a non-fungible token (NFT)? How will they impact the banking industry, and are they here to stay? In this article, we will dig into these questions.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?