Why NFTs are here to stay

9 December 2022

What is a non-fungible token (NFT)? How will they impact the banking industry, and are they here to stay? In this article, we will dig into these questions.

Let’s start by looking at the growth of NFTs in recent years. According to VMR1 the NFT market size was valued at $11.32Bn in 2021 and is projected to reach an estimated $231.98Bn by 2030. In addition, when it comes to royalty payments, a commonly used feature of NFTs, Galaxy Digital2 has estimated that at least $1.8Bn royalty payments have already been paid to Ethereum based creators.

These eye watering statistics show the sheer magnitude of NFT adoption and their very tangible emergence in financial markets. Notably, an element that has helped to catapult the appeal of NFTs is their applicability across industries including financial services, with new use cases constantly being explored.

What are NFTs?

NFTs are digital tokens created using blockchain technology that represent a digital asset. Examples of where digital assets are created as NFTs can be seen across industries including art, music, real estate in the metaverse, fashion, or in general a digital file holding data that is of value.

NFTs are particularly appealing because they:

- Are a unique representation of a digital asset that remains immutable once sold

- Create digital records of ownership and transaction history

- Provide integrity and authentication of digital assets

They are also non-fungible by nature meaning it is not easy to change them like for like. Money is the opposite, for example, you can take a £10 note and swap it for two £5 notes. When it comes to non-fungible assets, the asset itself holds unique value as one entity. This serves as a great mechanism to preserve originality. NFTs are commonly exchanged in the market by swapping them with something fungible, typically with cryptocurrency, the most common being Ethereum. This is done using a dedicated peer-to-peer NFT exchange platform.

Recently we have even seen fintech players such as Moonpay step into this space, offering platform integrations that can support NFT payments using payment methods such as Visa, Mastercard, Apple Pay. This is a trend we are seeing being picked up at pace to create a frictionless customer experience when buying and selling NFTs.

How is an NFT created?

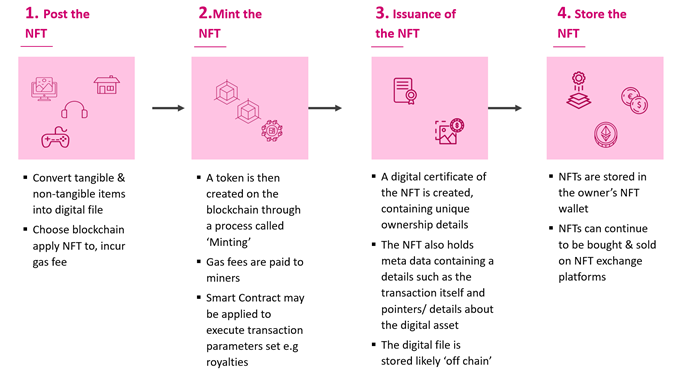

Figure 1: An illustration of the typical steps involved in the creation of an NFT using Blockchain

Whilst this process can feel quite complicated, the basic steps are summarised above. The journey starts when an NFT creator posts the digital file to a compatible blockchain of their choice using an NFT exchange platform. Think of this like putting an item up for auction. In turn, they will incur a gas fee—a nominal price allocated to blockchain miners who will carry out the coding required to create the NFT during a process called minting. Following this, the NFT can be issued and then stored in the owner’s wallet.

In addition, smart contracts are another feature of NFTs and when they are applied, contracts self-execute automatically at the point that an NFT is exchanged. They also retain information like transaction parameters, such as royalties. This makes it possible to apply a royalty fee onto a piece of art. For example, let’s say $5 goes to the creator each time the NFT is bought or sold. The self-executing contract simply means, if X happens, then Y must follow. If the art is sold, then $5 must be paid in ETH to the creator.

If you bought an NFT today, what you receive would comprise of the following: a digital token, which includes data about the token’s address and location on the ledger, a certificate that is issued by the NFT creator providing details about the digital asset and ownership, making this unreputable and ensuring authenticity of the transaction, and access to a digital file that is normally off-chain, meaning the location of the digital file is most likely not on the blockchain but typically on some form of cloud-based storage. NFTs are then stored in digital wallets which are held on distributed ledger technology (DLT).

Do NFTs have a future in banking?

NFTs are already gaining traction in financial services. Here are four considerations we think banks could embed into their Web 3 strategies.

- Frictionless banking

Tokenising digital creations has further business applications that could be useful to embed into financial products and services. Not only this but they could potentially be used to deliver improvements to banking operations. This presents various opportunities for banks and financial institutions to become market leaders.

Take the global payments provider Visa as an example. They have developed their own tokenised offering to remove friction when making online payments. Features of the offering include tokenisation of stored payment credentials, which can be shared across its network enabling more trust. In time, this could also help to prevent fraud by offering a level of immutability.

Visa and other industry competitors’ recent innovation led approach to tokenisation show how other firms could also benefit from exploring use cases for NFTs to level up frictionless banking options for customers. For example, a future use case could be around onboarding and KYC data that could be held as an NFT. This could make activities like opening accounts or loan origination a lot easier. Storing NFTs on DLT also decentralises information in a way that helps to promote operational efficiency in the long term. NFT certificates could then help customers gain more control over their data and how and where it’s used.

NFTs create opportunities for frictionless banking that will not just be delivered by the traditional financial services players. Unexpected entrants are embedding themselves into the world of NFT payment ecosystems, such as Instagram, Twitter, PayPal and LGTV. Their ability to create frictionless solutions on popular platforms, further enhanced by their ability to build a large community of followers, is certainly something to keep an eye on. The attraction for buyers and sellers to these platforms is strong and promises a customer base that could challenge customers amassed by traditional banks.

- Reduction of intermediaries and improved supply chains

Banking currently involves multiple intermediaries across the supply chain; however, NFTs have the ability to streamline these processes. For example, the tokenisation of mortgages enables some interesting benefits for mortgage processing. Mortgage lender, LoanSnap based in California, have already minted the first ever mortgage. Information can be stored as a digital asset containing applicant information, reducing intermediaries and the need for third parties alongside improving supply chain by making mortgage approvals a lot quicker.

Smart contracts could also be tied into mortgage or loan products held on NFTs. Loan terms and agreements could be weaved into NFTs and be executed automatically. This could reduce a number of associated fees and help distribute property or loans in a more effective way.

- Investments and fractionalisation

NFTs can be used to tokenise assets that private investors and everyday consumers want to acquire. Where people are willing to put their money is changing. To own a rare collectible in digital fashion or art is an indication that investor appetite and behaviour is evolving. A key question for banks would be, how to leverage the NFT movement?

Fractionalised NFTs (F-NFTs) are a feature allowing shared investment into large finance and debt structures by breaking an NFT into smaller pieces. LoanSnap allows retail investors to invest in a pooled structure of mortgages or housing debt, making it possible for anyone to own a fractional share of a mortgage. This is useful when considering green finance options as F-NFTs could expand the investment capability of adaptation and climate related projects by breaking up carbon credits.

- Brand loyalty and innovation

Banks will continue to encompass brand loyalty into their strategy when actively engaging various customer segments. NFTs can help evolve and enhance traditional brand loyalty offerings. There’s been an upsurge in communities and brands that promote NFT loyalty-based schemes, offering discounts, special offers and special merchandise releases that are backed by NFT holders, blending in a level of exclusivity across customer segments. We could apply this logic to banking — a bank account holder on a silver level reward current account which includes benefits and features such as travel insurance, discounts at certain restaurants, could be accessed using the account holders NFT. This would raise the profile of the bank and guide them into next generation banking using Web 3.

What should banks consider next?

There are of course limitations with NFTs in the current market. NFTs are not regulated which will naturally result in some reluctance. Also, high price sensitivity in the market makes it hard to stabilise the value of NFTs in the long term. This leads to other questions around what monetary value is pinned to an NFT if it’s also just a token representing an original asset. Banks would also need to consider how their customers might be expected to interact with NFTs – customers who are less tech savvy may not find them appealing.

This will limit the viability of transferring and facilitating purchases of NFTs linked to commodities through a banking platform for now but does not mean that a bank’s NFT journey ends here. The future of NFTs depends on their utility and how they are helping to solve real banking problems. Understanding the true potential and the use cases for Web 3 is important for banks to start doing now.

To explore how this aligns with your strategic focus, get in touch with our expert, Nina Bali.

References:

1Non-Fungible Tokens Market Size, Share, Scope, Trends & Forecast (verifiedmarketresearch.com)

2NFT Royalties: The $1.8bn Question | Galaxy

Related Insights

The role of regulators in accelerating Web 3 innovation

Financial institutions are seeing the potential that Web 3 technologies can offer but need the regulatory guard rails to have the confidence to commit.

Read more

Solving the KYC dilemma with Web 3

DLT has great potential to optimise Know Your Customer. We unpack the issues in KYC for retail and corporate banks and evaluate the application of DLT.

Read more

Blockchain opportunities for treasury – disruptive solutions or additional risks?

We take a look at how Web 3 is impacting investment banks, specifically bond issuance, intraday liquidity and in OTC derivatives.

Read more

Why Web 3 is too important for insurers to ignore

Web 3 has shifted from a buzzword to a mainstream competitive differentiator.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?