Emissions criteria in Australia’s National Energy Objectives: a guide to the implementation issues and key questions

20 November 2023

The revised National Energy Objectives come into force on 21 November 2023, addressing the energy trilemma by capturing the challenge of balancing energy reliability, price and sustainability. This will guide the regulatory policy decision-making of the Australian Energy Market Commission (AEMC) and the Australian Energy Regulator (AER). Decarbonisation will now be a core part of their work, becoming integral to their purpose and decision-making process.

The revised objectives also impact the industry, including how network businesses will undertake cost-benefit assessments to determine new investment under the Regulatory Investment Tests for Transmission and Distribution (RIT-Ts and RIT-Ds).

The long-standing debate on whether to include an environmental focus within the National Energy Objectives has now been settled. At a conceptual level, the final overarching framework is a sensible governance model in which:

- government will continue to have responsibility for establishing the strategic direction of energy markets including setting and revising emissions targets, and

- the AEMC and AER will be responsible for making and implementing rules that promote economic efficiency in the long-term interests of consumers, taking into account and balancing emissions reduction with the other criteria.

However, amending the National Energy Objectives and establishing the governance model is just the beginning. There are several difficult questions policymakers, market bodies and industry will need to grapple with to implement the new emissions reduction criteria.

The National Energy Objectives have been amended to incorporate a new emissions reduction criteria

In May 2023, Energy Ministers agreed to amend the National Energy Laws to incorporate an emissions reduction criteria within the National Energy Objectives. In September 2023, the Statues Amendment (National Energy Laws) (Emissions Reductions Objectives) Act 2023 received royal assent, and today the revised objectives take effect.

The National Electricity Objective has been revised to incorporate the emissions reduction criteria as follows (Point C, emphasis added):

The National Electricity Objective is to promote efficient investment in, and efficient operation and use of, electricity services for the long-term interests of consumers of electricity with respect to:

(a) price, quality, safety and reliability and security of supply of electricity, and

(b) the reliability, safety and security of the national electricity system, and

(c) the achievement of targets set by a participating jurisdiction -

i. for reducing Australia's greenhouse gas emissions, or

ii. that are likely to contribute to reducing Australia's greenhouse gas emissions

The National Gas Objective and National Energy Retail Objective have similarly been revised.

Recent and ongoing activities indicate the AEMC and AER are taking the necessary preliminary steps to implement the revised National Energy Objectives

Published in September 2023, the AEMC is now required to maintain a Targets Statement, outlining emissions reduction efforts across jurisdictions – this will be updated as necessary over time. The AEMC is also working through two rule changes to harmonise the new objective with network regulatory, planning and investment processes. This will occur through:

- the inclusion of emissions reduction within market benefits, within AEMO’s development of the Integrated System Plan (ISP) and for projects undertaking a Regulatory Investment Test for Transmission/Distribution (RIT-T/RIT-D); and

- the inclusion of an allowance for expenditure related to emissions reduction within the AER’s revenue proposals.

In September 2023, the AER published guidance on the application of the new objective to its relevant regulatory processes. This includes the regulatory determinations currently underway for several electricity distribution networks in NSW, ACT, Tasmania and NT. The AER also published its draft 2024−29 regulatory determinations for these distribution networks on the same day.

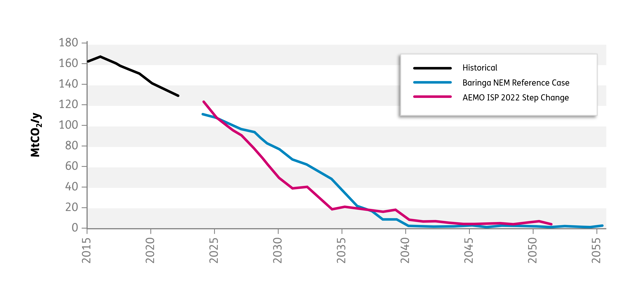

As outlined in Baringa’s latest NEM Reference Case, the revised national energy objectives come against the backdrop of declining NEM-wide emissions over the past few years. Baringa projects further reductions to occur, due to private and public sector decarbonisation commitments (graph below). The latter is encompassed within the AEMC’s Targets Statement.

Source: Baringa NEM Reference Case

The Commonwealth Government will provide critical guidance on the value of emissions reduction

The Commonwealth Government is expected to release the ‘value of emissions reduction’ (VER) this month. While there is limited public information on the scope of this work, we expect the VER to set out a methodology for how to monetise (i.e., value) emissions impacts associated with market bodies’ decision making, and potentially also publish this value (or set of values as the $/tonne price may change over time).

In the absence of an economy-wide emissions price in Australia to date, we have seen methodologies arising at a State/Territory level to quantify and value emissions impacts, including:

-

Social Cost of Carbon (SCC) (ACT Government) – the SCC measures the costs of damage from the release of one tonne of carbon dioxide equivalent (CO2-e). For the ACT, the SCC starts at a value of $20/tonne CO2-e from 2020-21 onwards, with an independent body to develop the SCC for application from 2025 onwards.

-

Cost-benefit analysis guidelines (NSW Treasury) – adopts a market price-based approach, setting the FY2023 price based on the average 2022 spot price of the European Union emissions trading scheme (converted to AUD), and applying an annual escalation factor derived from futures prices. The resulting carbon price for FY2023 is $123/tonne CO2-e, updated biannually.

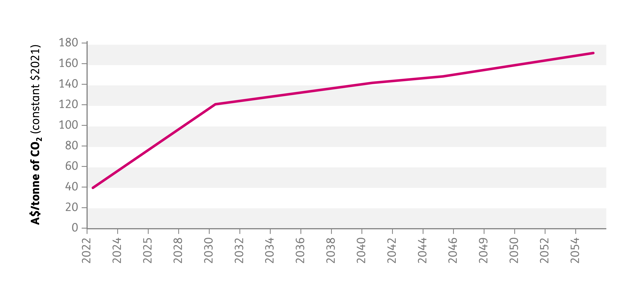

The ACT SCC approach informed Baringa’s Decarbonising Australia report, in which we modelled a 1.5°C Investor Credible Scenario that reduced emissions by 348Mt, valued at $43b of avoided consumer CO2-e costs by 2055. Our report highlighted, amongst other key findings, that timely investment in transmission will be needed to meet a 1.5°C-aligned scenario for the National Electricity Market (NEM). The ACT SCC approach also fed into Baringa's work on the value of transmission, with the SCC trajectory from that report shown in the chart below.

Source: Baringa's Clean Energy Investor Group report.

Notwithstanding the progress outlined above, there remains several questions policymakers, market bodies and industry need to address to implement the revised objectives

We’ve outlined and categorised these questions below:

Emissions scope and coverage

- What scope of emissions should be included? i.e., between scope 1 emissions (direct emissions) and scope 2 and 3 emissions (indirect emissions). Is a uniform approach to be adopted for every decision or is a case-by-case assessment to be made?

- What sectoral coverage of emissions should be included? For example, should transport emissions be included for energy reforms that impact electrical vehicle uptake, or should fugitive mining emissions be included for energy reforms that could impact future mining projects? Again, is a uniform approach or case-by-case decision made on sectoral coverage?

Resolving conflicts between competing considerations

- How are differing Commonwealth, State and Territory emissions targets considered in the assessment of national reforms? Where there’s differing levels of ambition between these targets, should the focus be on the Commonwealth target, the most ambitious target, the mid-point target or some other approach?

- How are the impacts of reforms that support achievement of one State’s emissions targets but hinder the achievement of another State’s targets to be considered? Due to different State emissions reduction targets, one State's VER may be higher than another's, which could result in sub-optimal decisions. For example, a proposed interconnector may increase emissions in State A by less than it reduces it in State B. If State A's VER is much higher than B's, then the interconnector's emissions impact (in dollar terms) is to increase costs and may make the project unviable, vs. an approach that applies the same VER in both States.

- How should different objective criteria be ‘weighted’ where this is a conflict? For example, a rule change that would improve reliability or security but result in a worse emissions outcome.

Qualitative assessment

- How are emissions impacts considered in qualitative (only) assessments?

Transitional arrangements for current or recent investment decisions

- Whether to take into account emissions impacts for RIT-T/RIT-D assessments that have already commenced? If so, should any additional consultation be done for those RITs where preliminary assessments excluding emissions have already been published?

- Whether to re-open any recent RIT-T/RIT-D assessments where construction has not yet commenced, if taking into account emissions benefits might be expected to materially change the outcome?

Ongoing announcements by the Commonwealth Government and policy makers should be anticipated and closely monitored by industry stakeholders

While this is by no means an exhaustive list, we hope it provides some material for consideration. We look forward to the Commonwealth’s VER work, and the work of other policy makers in this space, providing answers to some, if not all, of these questions.

Baringa are at the heart of some of the biggest programmes of change occurring in the energy sector relating to the transition to low carbon energy systems. We advise on policy development and detailed market design, business cases and impact assessments, policy delivery and technology change. Find out more about our work by contacting one of our experts below.

Related Insights

Demand-led SMRs: A 'government-last' model to power industrial growth through privately funded SMRs

Drawing on engagement with over 100 potential investors and deep analysis of UK energy market structures, this report sets out a 'Government-last' approach to SMR deployment.

Read more

Simplification, not suspension: why CS3D still matters for executive teams

CS3D timelines have shifted, but the cost, risk and opportunity remain. Learn why executive teams should act now to manage supply‑chain risk and value.

Read more

Carbon capture heats up in Asia: Will it cool down the planet?

Carbon capture’s rising role in Asia’s energy transition

Read more

From ambition to action: making the most of the Warm Homes Plan

An expert roundtable discussion on the UK Warm Homes Plan, exploring how government, local authorities and industry can deliver home energy retrofits at scale, reduce fuel poverty and accelerate low‑carbon housing.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?