Assessing and reporting on climate risks for the oil & gas market

27 June 2022

In this series of blogs, we share our insights on how climate change and the response to it will affect the oil and gas industry. And we’ll recommend how companies can analyse their risks, cut their operational emissions, and create low-carbon businesses so they can thrive through the energy transition.

In the previous blog, we looked at the biggest challenges facing oil and gas companies after COP26. Now, we turn our attention to how companies can measure and report on their current risk and future targets.

Oil and gas executives are facing many difficult questions – from governments, regulators, investors, customers, and their own employees. These include questions about the impact of climate change on the business, the impact of the business on climate change, and how to lower the risks and grasp the opportunities of the energy transition.

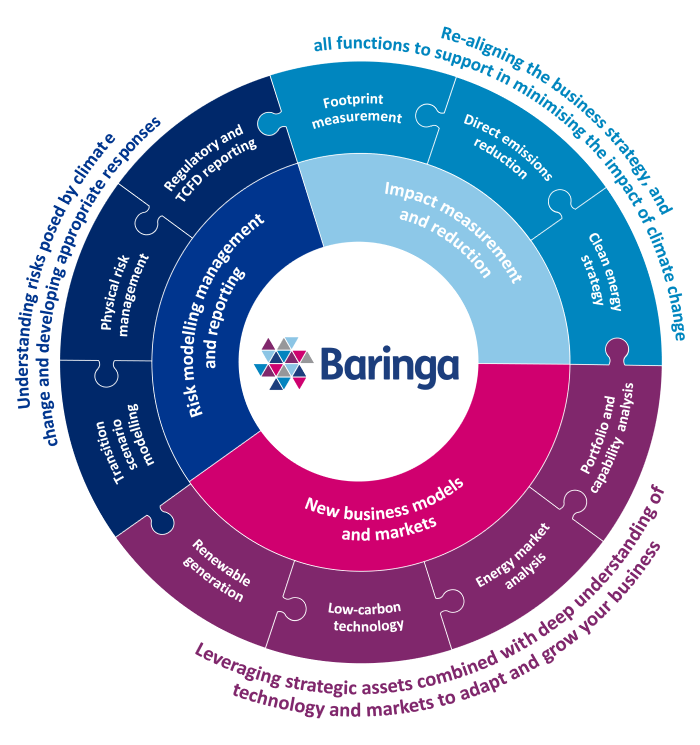

Baringa have worked with clients across the energy sector, government, and industry to refine our climate strategy framework and help you answer these questions. Our framework covers:

1. Risk management and reporting: we help you determine your company’s climate risk and the value that will be lost from your business.

2. Impact measurement and reduction: we help you evaluate how your operations are impacting the climate and what you should do about it.

3. New business models and markets: we help you assess opportunities to adapt your strategy and business model to reduce risks while making commercial returns.

Fig. 1: Baringa’s climate strategy framework

Let’s now look at the first challenge facing oil and gas companies: assessing the physical and transition risks. We’ll talk about impact measurement and new business models in our next two blogs in the series.

Physical risks are already here and bound to worsen

The oil and gas industry is already experiencing physical risks from climate change, and those are only going to increase.

The production and transport of hydrocarbons carry inherent risks which oil and gas companies work hard to mitigate. Installations onshore and offshore are designed to withstand severe weather events. But, as the climate becomes more extreme, new physical risks threaten these facilities.

The cost of these climate risks is significant. Some companies report costs of $500bn, in addition to $250bn of stranded assets.

Examples of these risks include:

• Rising sea levels and more frequent and severe storms. This leads to installations being evacuated, production shut, and revenue lost. ConocoPhillips estimates that if all Gulf Coast business unit production was shut down for three days, it would lead to $35m in lost revenue, based on the 2019 average realized price of $48.78/boe. With WTI prices currently between double and treble those in 2019, and a projected busy hurricane season in 2022, a similar three day loss today would cost over $100m.

• Extreme drought. The western US is experiencing exceptional drought affecting water levels. The onshore natural gas industry uses significant quantities of water for fracking, and many wells are in the areas affected by the droughts.

• Melting permafrost in the Arctic. When the North Slope was developed over 40 years ago, casing for wells was set directly into the permanently frozen soil. But, as warmer weather thaws that soil, it is impacting the integrity of wells.

Transition risks are complex and ever-evolving

With the shift to a low-carbon economy, fossil fuel may no longer generate the same returns. This transition risk is hard to measure, with many questions to answer:

• Will the energy transition be orderly or disorderly? A disorderly transition makes investment decisions difficult.

• What will oil and gas cost in these scenarios? If national oil companies decide to produce their hydrocarbons while there is still a market for them, how will that affect prices? The IEA forecasts crude oil to reach $35/bbl as soon as 2030 in their net-zero pathway.

• What will happen to the price of carbon? Norway is raising prices to $237 per tonne CO2 in 2030. The Bank of England Late Action (disorderly scenario) forecast $30 per tonne in 2030, rising to $1,000 per tonne in 2050. Many oil and gas companies test their investment cases at only $100 per tonne.

• How will demand change? As renewable energy becomes cheaper than hydrocarbons,

the transition might accelerate. For example, Norway plans to phase out cars with internal combustion engines by 2025, but current predictions see it hitting zero as soon as 2022.

Understanding your risks

Many oil and gas companies struggle to measure and report on the climate impact of their investments, or the climate-related risks of their assets. They also can’t demonstrate to their investors that their values align.

Using 20 years of experience in advising governments, energy and financial services clients on the energy transition and climate change, Baringa developed a Climate Change Scenario Model (CCSM), which was acquired by BlackRock in June 2021. We are continuing to work together to set the standard for modelling the impacts of climate change and the transition to a low-carbon economy.

Get in touch to better understand the climate-driven risks and impact on your portfolio under different climate scenarios.

Join us next time when we look at how oil and gas companies can measure and reduce their emissions.

Related Insights

Synchronisation of the Baltic power system with Continental Europe opens exciting opportunities for batteries

The synchronisation of the Baltic power system with continental Europe is a significant milestone that opens exciting opportunities for batteries.

Read more

Renewables Market Scanning Report

Which are the most attractive markets for investing in renewable assets globally?

Read more

How can investors and developers capitalise on South Korea’s evolving energy market?

South Korea's energy market is transforming in line with the global shift to renewable energy.

Read more

How ‘Equipment-as-a-Service’ models unlock commercial decarbonisation

Read our latest piece, created in collaboration with Tallarna, to explore the components of an ‘Equipment-as-a-Service’ model, how they can be deployed, and how to increase take-up.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?