Transition Finance – It’s not enough to just invest in green

3 July 2022

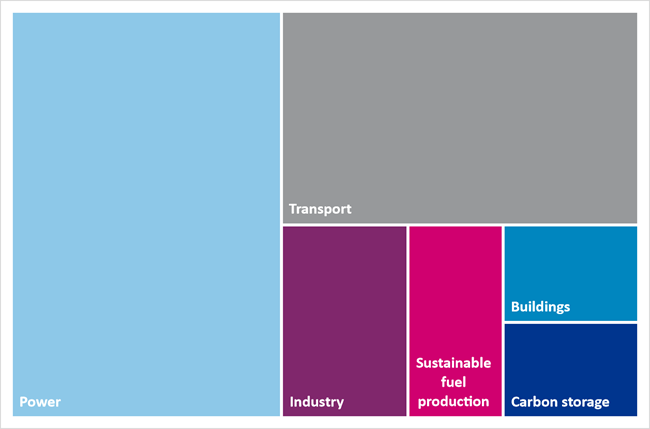

We estimate that around $350tr of capital1 is needed globally to support the transition and limit global warming to 1.5 degrees. The majority of this investment will need to be allocated in the Power and Transport sectors, in particular to expand and scale new green technologies due to their material impact on carbon emission reduction.

2021 to 2050 incremental cumulative investments to reach a 1.5°C scenario (compared to a 4°C scenario); Source: Baringa/Blackrock

Current figures exclude financing of Agriculture, Forest or Land Use where material investment is also required.

"Investing in green alone will not achieve the radical change required - only through a systemwide transformation will we be able to achieve a just and successful transition to net zero."

Emily Farrimond

As we’ve highlighted before, there is a need for a Just Transition, which can only be achieved through a conscious consideration of the broader environmental and social impact of new funding and projects, as well as the social hierarchy of green vs brown investments.

Transition finance holds the key to unlocking the funds needed to support high emitting industries to shift gears and make a real difference in achieving net zero objectives.

What is Transition Finance?

Transition finance seeks to help companies, particularly those in high emitting sectors, to align with the Paris Agreement 2030 and 2050 goals by providing the capital needed to facilitate progressive emission reductions.2

Transition finance is intended for economic activities that are emission-intensive that do not currently have a viable green substitute – technologically, economically or both – but are important for socio-economic development and environmental sustainability. An example of this supporting organisations with carbon intensive assets to reduce and minimise their emissions through the adoption of green technologies, such as an oil and gas company seeking to decarbonise and switch to renewables.

Is green the new black? The funding gap

Over recent years, investors have had a clear focus on assets classified as green, resulting from a greater social and environmental conscience, combined with increased ESG regulation and transparency around financial risks labelled as sustainable.

Green finance is now an established asset class. As an example, green bonds alone reached a total of more than $500bn of debt issuance3 during 2021 and are expected to reach $5tr by 2025 according to the Climate Bond Initiative4. This move to green financing has been followed by social and sustainability linked lending instruments which are emerging as subcategories of sustainable finance.

This is a great start; however, the same success has not translated to transition finance which is seen as a riskier alternative to green financing. We believe the reasons for this include:

- Greenwashing risk: ESG-conscious investors are wary of funding “no-go” industries or activities, with many having pledged to divest in order to avoid increased reputational risk. It is harder to explain to your investors why you are financing an oil rig vs a solar panel farm, even if your funding has a dedicated decarbonisation purpose. This can be seen to carry too much risk for financial institutions.

- Lack of standardised labelling for transition finance: Despite literature being published by industry bodies on climate transition finance, there are no guiding principles or standard definitions. Some even argue whether there is a need for such a category, as the existing green/social and sustainability linked instrument should be able to accommodate the highly emitting sectors.

Why should you care about transition finance and a ‘just transition’?

There are three primary reasons why transition finance is important for financial services firms.

- Business opportunity: Out of the $350tr worth of investment required to reach a low carbon economy, many of these opportunities will not be classified as green if we use the EU Taxonomy example. These investments however are still essential, either for the future or as an interim solution until green technologies are deployed. Market players are seeking to capture this opportunity, with regulators encouraging investments that are not only green but “greener”.

- Increased interest from investors, private equity and asset managers to capture the transition finance opportunity: Two examples include Brookfield, who has set a $15bn Global Transition Fund and announced plans to grow their energy transition business to USD 200bn5; and BlackRock, who will be launching their Energy Security and Transition Infrastructure Fund.

- Regulatory pressure: The Platform on Sustainable Finance has published a Final Report7 to extend the EU Taxonomy “beyond green”. If this proposal is adopted, it could become the new Transition Finance Taxonomy.

- The only road to net zero: During 2019, according to the IEA8, industry was the largest emitting sector making up more than 40% of total emissions9. This sector needs to not only remove its dependency on fossil energy but also innovate low carbon production processes10. Achieving the Paris decarbonisation target will not be possible without these high-emitting sectors transitioning, hence the need to focus not just in green but in brown too.

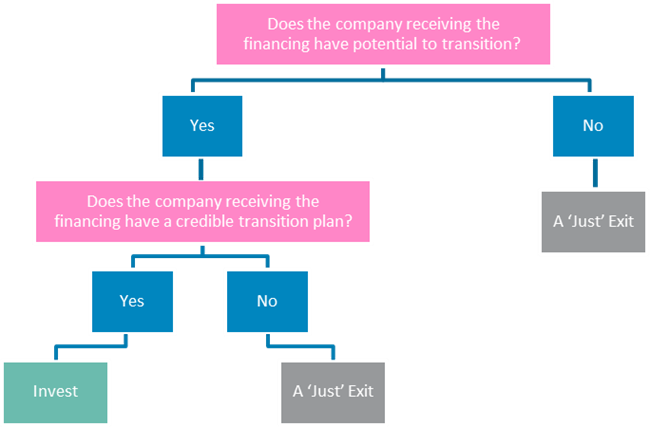

The transition can be achieved by taking a science-based objective approach when deciding which companies have genuine potential to transition and if so, either

- Set credible transition plans or

- Plan a “just” exit decommission strategy

The transition finance decision tree; Source: Baringa

Those financial institutions which take this approach will transition their own businesses and portfolios to achieve their own decarbonisation commitments, while at the same time helping the transition.

- Social outlook: While the environmental agenda, and in particular green investments, have often been a priority in the sustainable finance “social hierarchy”, there is now a deeper understanding on the topic and acknowledgement of the need to apply a social lens to balance all objectives. A successful transition is one that is just, and where the responsibility and costs are shared amongst all stakeholders, particularly protecting the most vulnerable - a ‘Just Transition’. For example, when an oil and gas structure is dismantled for good, there should be a focus on how to redeploy the teams on the ground so they can continue to be employed, and that the economic impact in the local area is minimised through alternative investments in the community.

As the timeline to deliver those net zero commitments gets closer and more real, paired with the pressure from regulators and industry events such as COP27, we expect transition finance to increase its relevance to both companies and market participants. Despite the difficult environmental and social implications on transition finance, this as an opportunity for investors to incorporate systematically blended social and environmental decisions. This will allow the real economy to not only be greener, but more sustainable and inclusive, securing backing from the economy as a whole.

"This can seem a daunting step for organisations who are just getting their heads around green, but not accepting transition finance as a viable investment will result in a missed opportunity for the organisation and the planet and its people."

Natalia Cermeno

We’d like to thank Xingliang Fang and Baringa’s global transition team for their input into this article, specifically in estimating the size of the opportunity to a low carbon economy.

References

1 Baringa/BlackRock

3,4 Climate Bond Initiative (April 2022) “Sustainable Debt Tops $1Trillion in Record Breaking 2021, with Green Growth at 75%”

5 Buyouts Insider (February 2022) “Brookfield looks to grow energy transition business to $200bn” , IPE Real Assets (June 2022) “Brookfield raises $15bn for maiden energy transition fund”

6 Investment Week (June 2022) “BlackRock targets energy transition with infrastructure strategy”

8 IEA (2021), “Greenhouse Gas Emissions from Energy: Overview”, IEA, Paris.

9 Total emissions calculated by allocating electricity and heat emissions to each of the final sectors. Final sectors defined as Industry, Transports, Building and Others.

10 World Resource Institute. Max Ahman “Perspective: Unlocking the “Hard to Abate” Sectors”

Related Insights

Future-proofing climate disclosures: Leveraging climate reporting for nature

Forward-thinking companies are integrating climate and nature into their strategies to drive innovation and resilience.

Read more

Transition planning in turbulent times: How financial institutions can adapt and lead

The shift to a low-carbon economy is challenging for financial institutions; we explore how they can adapt and lead in today's tough landscape.

Read more

Simplification Omnibus: what you need to know and where to go from here

We share what the Simplification Omnibus means for CSRD, CS3D and the EU Taxonomy and how you should respond.

Read more

2025 Outlook: What lies ahead for climate and sustainability in financial services?

Here's what's front of our minds for 2025 based on our dialogue with, and work for, climate and sustainability leaders across financial institutions.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?