Building a reliable net zero transition plan

1 April 2022

COP26 has put net-zero transition further up CEO agendas, if that were possible. Nowhere is this truer than for physical commodity supply chain and trading organisations. Big open questions remain on how prepared for the transition these complex organizations with a global reach truly are.

In this blog we’ll explore some of the gaps we see and how we are supporting our clients in closing them on their journey to develop – and deliver – more reliable, credible and robust net-zero transition plans.

Transition planning has not just landed in the sector. Commodity supply chain owner-manager-optimisers – as in other impacted sectors – are already acting and announcing their plans to decarbonise operations and deliver net-zero emissions by 2050. As the pressure from banks and investors ratchets up, plans have been published and scrutinized.

How ambitious and achievable these plans are, is now the hot topic for industry participants. Broadly the debate can be broken down into three key topics:

- How have net-zero transition plans been calculated/baselined (and therefore what does actual success look like)?

- How affordable is the planned transition for investors/shareholders?

- How will organisations effectively measure, manage and capitalise upon the inherent risks and opportunities these plans create for their day-to-day operations and profitability?

The organisations that can address these questions most effectively will, ultimately, have a competitive advantage. But where to start…?

Closing the gap(s)

Commodity trading companies have been publishing and updating their net-zero plans and strategy for a while now, but most, if not all, do not satisfactorily resolve the following gaps:

Clarity on CO2e emission accountability and alignment on calculation methods – covering all three scopes of emission.

Many published transition plans do not state the amount of CO2e that they are accountable for and therefore have no clear benchmark against which to ‘achieve’ net-zero; The methods and assumptions used to calculate need to be clear and transparent to ensure an organization’s plan is credible. Introducing scope 3 emissions represents the biggest challenge here as the number of impacted supply chain participants and activities can grow exponentially.

For example, when Company A purchases a FOB cargo of copper concentrate from Chile, ship it to Taiwan and blend it with a shipment of their own product, to what extent are they accountable for the upstream CO2e emissions of mining and transporting the third-party material to the port? How do they put a footprint on that product when they sell it? If they wish to offset those emissions, how do they get sufficiently accurate data?

Some organizations take a clear view on this. Many do not. Ultimately, there is no common agreement across the sector to drive consistency.

Reliable emissions data and portfolio assessment.

Completing an end-to-end mapping to “nail down” all the data and, consequently, the specific amount of emissions that a company is accountable for can be a very labour intensive and costly activity. However, mapping and making it clear where the key data points will be set across the different commercial use cases will bring more confidence that reliable data is being sourced to map your carbon footprint.

Also, it will help the company to model this data and demonstrate the evolution of their portfolio to support how they will achieve a sustainable net-zero based on different transition scenarios – i.e. current, rapid or radical.

Specifics on delivery

Commodity traders are struggling to outline how planned reductions will specifically be achieved, their delivery roadmap and the initiatives they are pursuing in the short and medium-term. Those organizations that do attempt this commonly do not make clear how they will transform their commercial model, their operating model, nor their technology estate to enable the offset or direct reduction of emissions. Where they do, the underlying economics of their transition plan can quickly unravel.

Current Economics

Investors need to be convinced that commodity supply chain owner-manager-optimisers will maintain margins and profitability despite the strong premiums to go ‘green’. The economics of replacing current fuel in logistic chains with zero-carbon alternatives are challenging.

Table 1: Green premiums to replace current fuels with zero-carbon alternatives

| Fuel Type | Retail price per gallon (US average 2015-2018) |

Zero-carbon option per gallon (current estimate price) |

Green Premium |

|---|---|---|---|

| Gasoline | $2.43 | $5.00 (advanced biofuels) $8.20 (electrofuels) |

106% 237% |

| Diesel | $2.71 | $5.00 (advanced biofuels) $8.20 (electrofuels) |

103% 234% |

| Jet fuel | $2.22 | $5.00 (advanced biofuels) $8.20 (electrofuels) |

141% 296% |

| Bunker fuel | $1.29 | $5.00 (advanced biofuels) $8.20 (electrofuels) |

326% 601% |

Alternative energy sources to reduce the energy intensity of supply chains are, conversely, land-intensive – creating knock-on environmental challenges.

Table 2: Renewables are intermittent and need more physical space to generate as much power as fossil and nuclear alternatives

| Energy Source | Watts per square meter |

|---|---|

| Fossil fuels | 500 - 10,000 |

| Nuclear | 500 - 1,000 |

| Solar | 5 - 20 |

| Hydropower | 5 - 20 |

| Wind | 1 - 2 |

| Wood and other biomass | Less than 1 |

Technological advancements such as CCUs (Carbon Capture, Utilisation and Storage) and/or DAC (Direct Air Capture) may provide the solution, but at what price?

| Technology | Costs per tonne of CO2 |

|---|---|

| CCU 1 | $39 - $194 (capture, transportation and storage costs) |

| DAC 2 | $200 – $600 (still very expensive due to the amount of energy necessary in the process) |

1 https://www.iea.org/commentaries/is-carbon-capture-too-expensive

2 https://www.wri.org/insights/direct-air-capture-resource-considerations-and-costs-carbon-removal

Transparency equals credibility

Arguably most important, industry players need to establish and champion the capability to report outcomes and progress. Transparency will increasingly be a (the?) key commodity for commercial and investor relationships – securing reputations and credibility (and financing) in the sector. NGOs and other market influencers remain to be convinced with the likes of Greenpeace questioning key industry participant figures and accounting methods.

More importantly, banks, investors, insurers and customers are much better informed and asking much tougher questions. Net-zero is raising reputational risk on the corporate risk register. Negative news and brand perception will only increase pressure on financial institutions to place a significant premium – or in the worst case – withhold finance for CAPEX projects and day-to-day operations.

Where to start? Set direction, build foundations, protect (and grow) value.

Establishing a credible net-zero transition plan that aligns to your commercial strategy, considers – and challenges – your operating model, and achieves meaningful emissions reductions across global supply chains is a complex problem to solve, to say the least.

Based on our experience of working with the leading commodity trading companies in the world, we recommend that you start by setting a very clear direction for your business. Those that look set to survive and thrive in the net-zero world begin by asking themselves a simple but fundamental question: ‘how do we win’ in the new world?

The answers differ, but there are four common themes that we observe:

- They ensure their net-zero strategy – and their net-zero transition plan – is at the heart of their commercial strategy.

- They understand the footprint of their business activities at a highly detailed level, and build that understanding into decision making throughout the organisation.

- They recognize the criticality of delivering an operating model that is in lockstep with how they plan to generate and protect margin in the brave new world of carbon taxes and product footprints, and they build the foundational capabilities needed to enable this.

- They focus on the long-term value, not short term-costs, accepting that net-zero is inherently a long-term commercial challenge that has upside potential to create competitive advantage and new sources of revenue, and that a credible plan will guarantee access to cheaper capital funding to make the transition.

What Next?

With our deep sector expertise and broad delivery capabilities, we have been helping physical commodity supply chain and trading organizations for over 20+ years to achieve commercial clarity and operational model alignments, improve their digital maturity and adapt and ensure they maintain growth and agility.

This places us in a unique position to support our client partners to define and deliver an holistic, achievable, long-term solution to the net-zero transition challenge - underpinning (and informing) their commercial strategy - to deliver genuine emissions reductions, protect long-term business value, and to ultimately deliver a reliable and credible transition plan.

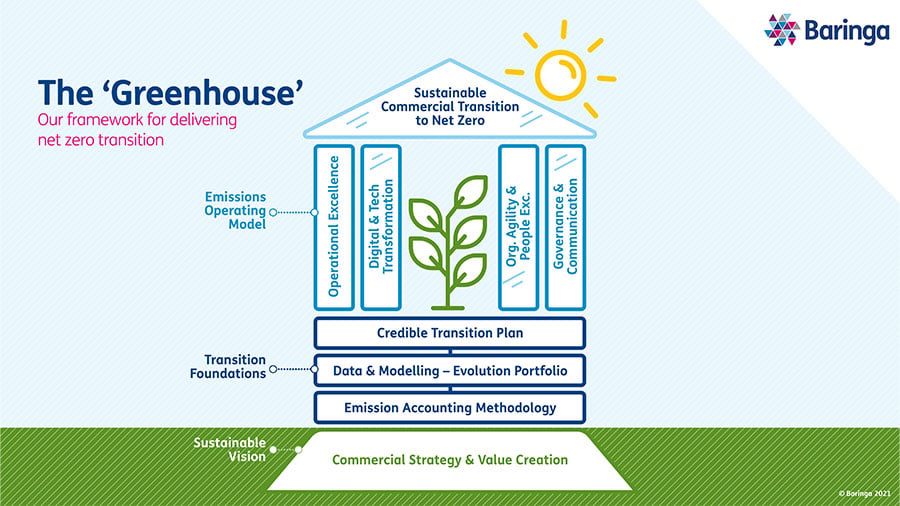

In the coming weeks, we will share a series of blogs that explore in more detail each element of the climate transition framework (aka. The Greenhouse) we have developed, from the foundations your business needs to shape and communicate your net-zero plan, through to the complex implementation of the operating model, processes, organization and governance that will see it delivered.

If you have any perspectives or questions on this blog please reach out to the team, we’d welcome your insight.

For more information please get in touch with a member of the team:

Bernardo Ribeiro, Expert in Commodities & Trading, bernardo.ribeiro@baringa.com

Paul Stewart, Expert in Commodities & Trading, paul.stewart@baringa.com

Tibor Horvath, Expert in Commodities & Trading, tibor.horvath@baringa.com

David Kane, Partner, Commodities & Trading, david.kane@baringa.com

Related Insights

Demand-led SMRs: A 'government-last' model to power industrial growth through privately funded SMRs

Drawing on engagement with over 100 potential investors and deep analysis of UK energy market structures, this report sets out a 'Government-last' approach to SMR deployment.

Read more

Simplification, not suspension: why CS3D still matters for executive teams

CS3D timelines have shifted, but the cost, risk and opportunity remain. Learn why executive teams should act now to manage supply‑chain risk and value.

Read more

Carbon capture heats up in Asia: Will it cool down the planet?

Carbon capture’s rising role in Asia’s energy transition

Read more

From ambition to action: making the most of the Warm Homes Plan

An expert roundtable discussion on the UK Warm Homes Plan, exploring how government, local authorities and industry can deliver home energy retrofits at scale, reduce fuel poverty and accelerate low‑carbon housing.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?