Evolving liquidity risk management in the post-stress environment

23 October 2023

Last year's liquidity crisis, driven by market price volatility and spikes in global energy prices has caused heightened margining demands from clearers and exchanges. As a result, many energy and commodity players have set up some form of liquidity risk management within their organisations. It’s easy for market participants to believe they’ve weathered the storm, but complacency should be avoided. In light of geopolitical uncertainties, it’s wise to further strengthen liquidity frameworks to better cope with tail-risk.

During the last year many firms have set up liquidity risk functions, introducing margining risk KPIs and reporting, but also going as far as introducing margining limit frameworks. We elaborated on the impact of this market turbulence and on the risk framework of energy trading firms in our whitepaper published earlier this year.

The market seems to have slowed down from peak mayhem, although we are still seeing elevated flat price levels and relatively high levels of volatility. Whether the market is sending signals of decreased overall risk in commodity markets or we’re perceiving a false sense of security remains to be seen.

One could argue that the industry has returned “back to normal”. However, this “normal” is characterised by strongly increased interest rates, a global slowdown of economic growth and stagflation signals from some of the strongest economies. On top of this, the geo-political environment remains extremely unstable as evidenced by recent events in the United States and the Middle East. The combination of the economic and geo-political landscapes has resulted in significant uncertainty in global energy demand and supply.

Given this, can commodities trading organisations really let liquidity risk out of their sight? Our answer is no; while it is easy to be lulled into a false sense of security, the global landscape is complex and fragile. Organisations need to be prepared for further price and volatility shocks; especially taking into account the cost of margining. Organisations should take the opportunity now to further strengthen and prepare for what may lie ahead.

By implementing rudimentary liquidity risk frameworks whilst in crisis response mode, there are two areas that many firms have not paid attention to:

- Elevating the liquidity risk management into strategic risk capital planning on a firm level to ensure resilience in case of extreme market events.

- Focusing on managing liquidity risk, and steering trading activities and related liquidity usage levels in line with commercial objectives.

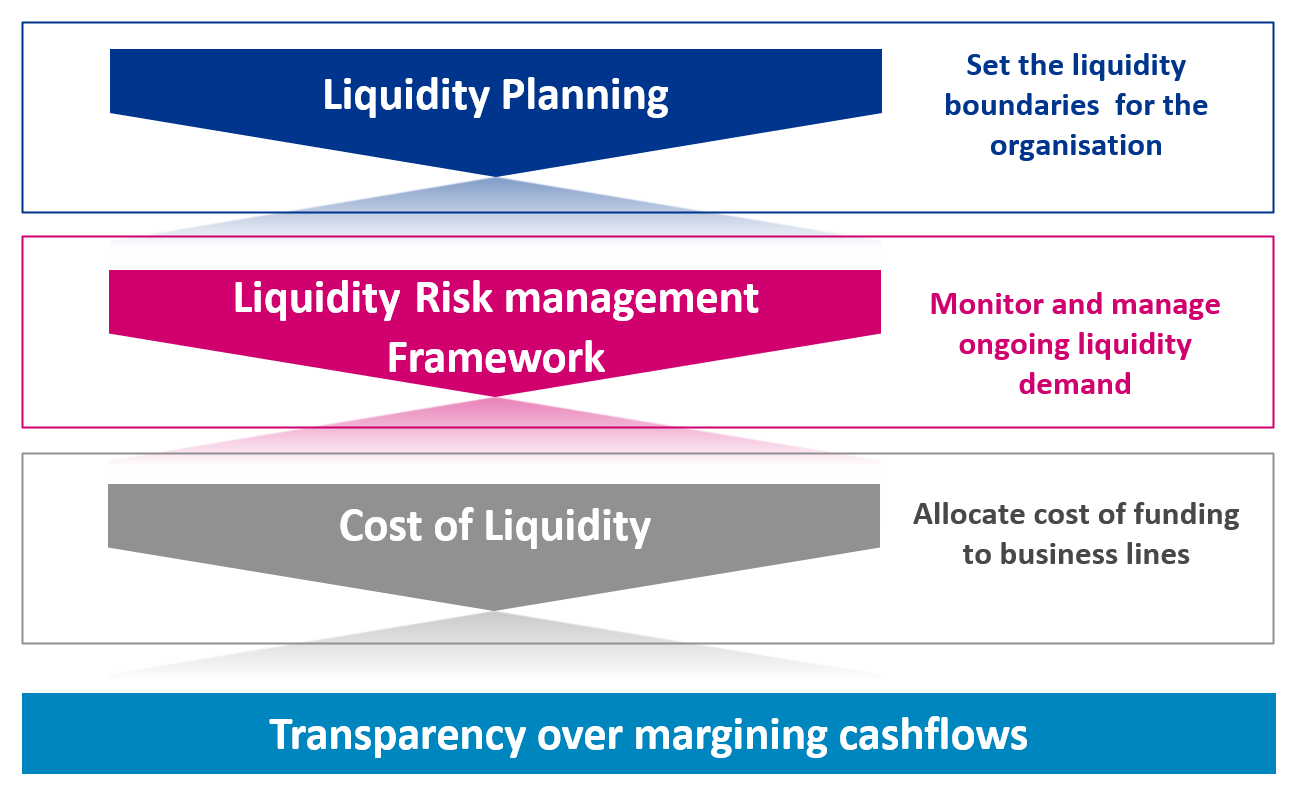

Liquidity Risk capital planning

In order to include margining risk within the overall liquidity risk capital planning of organisations, firms have to introduce margining risk stress-testing into the yearly business and risk capital planning. This is no different from applying stress scenarios and testing to market risk and ensures the robustness of the liquidity risk management. For this firms need to establish:

- Global price stress-scenarios relevant for their portfolios and future strategic objectives and apply these to all risk types (market, credit, liquidity, physical, etc.)

- Initial and Variation margin simulation capabilities to calculate impact of price-stress, volatility jumps and correlation breaks.

- A view of their future trading portfolio/ hypothetical portfolio based on desired hedge levels including trade products, and composition of asset classes as well as assumptions around the split between cleared and un-cleared derivatives trading. This might very well necessitate a review of current hedging levels and policies to obtain the most adequate portfolio position.

Based on the input parameters, firms will have to simulate Initial Margin (IM) and Variation Margin (VM) for the organisation-wide stress scenarios to gain understanding of maximum peak liquidity outflows for the coming business year. With the changes in the trading portfolio, this will result in simulated IM and VM outflows for different time horizons.

The aim of this exercise is to identify the funding gap that needs to be held as an additional liquidity buffer on top of standard risk capital. In order to calculate this funding gap, a base case scenario simulation with the un-stressed price assumptions should be run, to find the difference, between the base case and the stress-scenario Treasury departments should be responsible for determining and securing the short-term funding sources needed to fill this funding gap.

Access to affordable funding sources as well as the appetite for net interest-bearing debt (NIBD) may be limited, which needs to be considered during the planning.

Steering of liquidity risk exposure

The liquidity risk steering differs slightly from the steering of Credit and Market Risk exposure, in that a base demand of liquidity will always be caused by derivative trading activities (either through exchanges or through bilateral arrangements with a margining obligation). Firms cannot aim to just minimise their financial liquidity demand, as the best answer to this would be to simply stop trading.

Organisations need to have a holistic commercial view and aim to optimise the liquidity demand required to run their current or future portfolio. For this reason, liquidity risk steering will require a complex limit framework, including:

- Dynamic limit re-allocation principles, to enable activities to shift, either towards portfolio optimisation, exposure reduction or to support changes in strategy and even to go as far as considering the trading of available liquidity limits between desks to ensure best use of capital for return creation.

- Setting various KPI’s to gain visibility of liquidity exposures - on commodity level, strategic portfolio level as well as on company level.

- Embedding the cost of liquidity into the steering framework, to support balancing decision making between Credit, Market and Liquidity risk, and to include liquidity charges in trader incentives and performance evaluation.

Considering the dynamics at play, there is no out-of-the-box solution for any organisation. What is needed is a tailor-made framework that takes into account the firm’s business model, the state of maturity of the risk management functions, available skills, capabilities, tools and resources as well as strategic priorities.

If you’d like support with liquidity risk, Baringa is ready to help. For more information, please get in touch with us.

Our Experts

Related Insights

Unlock the key to successful trading transformation

Discover how Baringa helps energy and commodity businesses deliver faster, lower-cost change with lasting impact.

Read more

Navigating the ETRM and CTRM landscape: trends shaping smarter technology decisions

In this article, we demystify the complexity and look at trends that will help you make more informed decisions.

Read more

What capabilities do you need for the trading organisation of tomorrow?

Why commodity trading transformations fail and how a capability model sets teams up to deliver.

Read more

How to solve the data paradox in commodity trading

Implement successful change programmes that modernise operations, enhance performance and position your commodity trading business for long‑term growth.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?