Overcoming greenhushing: greenwashing risks in sustainability-linked loans

6 December 2022

It is becoming increasingly clear that the transition to a more sustainable, lower-carbon society is not happening fast enough. A recent report by the Intergovernmental Panel on Climate Change said that the window to keeping global warming to 1.5°C is fast closing and that delaying emissions reductions puts that target, as well as a 2°C target, out of reach1. There is a need for financial institutions to fully understand the impact of this and develop financial products to help navigate the transition in a way that minimises the risk of greenwashing.

This requires a significant shift in the way financial institutions operate, going beyond industry frameworks and guidance to meet clients' needs. They will need to build transparency and credibility with key stakeholders, customers, investors, governments, and regulators, while equipping themselves to be fit for future challenges.

The increase in sustainable financing, such as sustainability-linked loans (SLLs), is driving the much-needed capital allocation for a transition to a low-carbon economy. However, the lack of a global standard, inconsistencies in reporting and approaches from both borrowers and lenders, as well as a lack of transparency increase the risk of greenwashing from all actors involved in such transactions.

We carried out an analysis on the issuance of SLLs, this was a refresh of similar research that was conducted last year. In our 2022 review, we found that:

- The types of lending have changed compared to last year from general purpose lending to specific finance

- There has been an improvement in the ESG objectives of the SLLs being publicly disclosed

However, there is not enough transparency on the borrowers’ transition plans and their interim targets, leading to ‘greenhushing’, a term used to describe when companies choose to omit details of their climate-related targets in order to avoid public scrutiny2.

The rise of sustainability debt issuances

Given the capital required to transition to a low-carbon economy, it’s no surprise that the sustainability debt issuance market has seen a tremendous uptick in recent years. Data from Bloomberg’s New Energy Finance states that the total issuance of sustainable debt products rose to US$1.64 trillion in 2021, from US$28.7 billion in 20133. In particular, the issuance of sustainability-linked loans, grew to US$322 billion in September 2021, from US$6 billion in January 2016, which represented 20% of the sustainable debt market in 2021 compared to 4% in 20164. SLLs are intended to mobilise capital towards sustainable outcomes and are often tracked as part of banks’ sustainable finance targets aligned to that objective.

A stricter regulatory landscape

Regulators around the world have made it clear that ESG is on their agenda and that it’s here to stay. Some of the most prominent sustainability regulations include the European Union’s Sustainable Finance Disclosure Regulation, the EU Taxonomy, the UK's Sustainability Disclosure Requirements, and the upcoming international guidance set by the International Sustainability Standards Board. These regulations have a common thread mirrored by the strategic objectives of the UK's Financial Conduct Authority (FCA) to make markets function well by increasing transparency on the sustainability profile of products and firms, and reduce the risk of harm arising from greenwashing5.

Alongside global or national regulations, countries have begun to look at sustainability claims more closely and publicly showcasing when a firm's advertisements have been misleading. In October 2022, the UK FCA proposed stricter rules to tackle greenwashing by placing restrictions on how sustainability-related terms such as ‘ESG’, ‘green’ or ‘sustainable’ can be used, as well as more detailed disclosures for retail and institutional investors6. The regulator will also be revamping its supervisory engagement on sustainable finance and enhancing its enforcement strategy.

The Australian regulators have issued a guidance that relies on existing legislation to tackle greenwashing. Echoing the UK’s ambition, the Australian Securities and Investments Commission conducted a sample review of fund managers and superannuation funds providing sustainable investment offerings. The regulator noted that when offering or promoting sustainability-related products, financial institutions should ensure that they are using clear labels and define sustainability-related terminology, as well as provide clear explanations as to how sustainability-related considerations are factored into investment strategies7.

Monitoring loan outcomes

The heightened risk of greenwashing for SLLs may occur when the disclosure of the contractual detail is low, and often with considerable differences in the information that is disclosed. On top of this, there are limited or no market-level mechanisms to effectively assess and monitor that the financed activities deliver the intended outcomes of the SLL. Our research found that there are alarming discrepancies on what borrowers and lenders share regarding the loans, and thus, auditing the outcomes poses difficult. A question arises as to who should be monitoring the outcomes of the loans, and what are the consequences for non-compliance?

Stakeholders need to be aware of greenwashing risks and how to identify, assess and mitigate these from a lender and borrower’s perspective, and should enforce more transparent and systematic disclosures. Financial institutions can also evaluate the performance of SLLs against their ESG targets, coupled with a thorough understanding of the regulatory landscape. This insight can help lenders and borrowers to better understand the risk of greenwashing, and how it can be mitigated.

Methodology: Our criteria for analysing SLLs

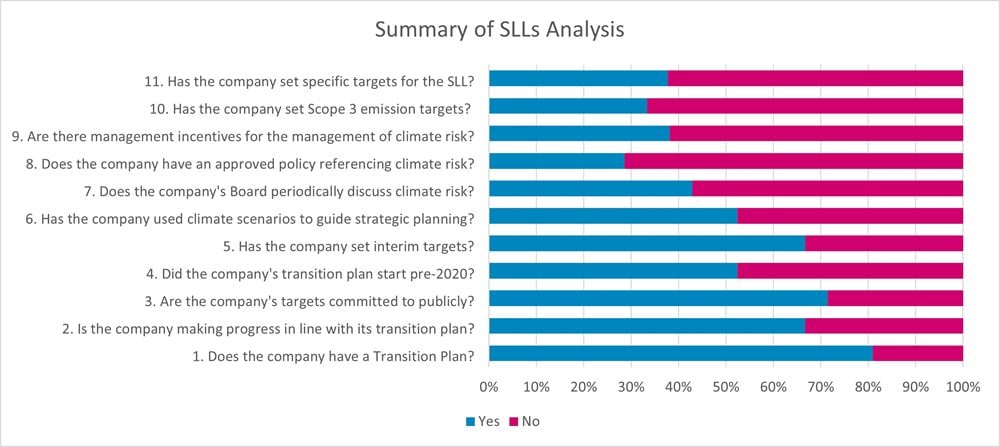

To identify if a particular loan has a risk of greenwashing, we conducted proprietary research on a sample of SLLs, reflecting US$12 billion in loans from a diversified pool of large, multi-region corporate borrowers. As seen in the research we conducted in 2021, there is limited publicly disclosed information on the loans. Our findings show that there has been a decrease in transparency in the borrowers’ disclosures on climate change. Our research highlighted that:

- Almost two thirds of the borrowers in our sample didn’t have a CDP report

- 81% of the SLL borrowers had a Transition Plan

- 67% of the borrowers had interim targets in their Transition Plans

- 33% of the SLLs revealed their scope 3 emissions targets, reflecting a 13% increase compared to last year

- Almost 60% of companies did not incentivise their Boards and Executive teams on climate risk management and achieving targets

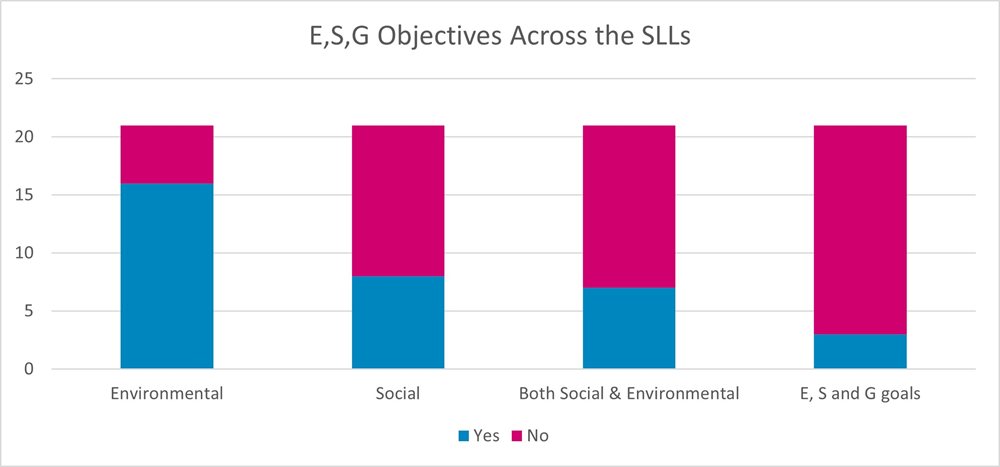

Our updated research also found that the type of loan has changed, compared to 2021. SLLs have shifted from general purpose lending to specific project finance. More specifically, there’s been an increased focus in the loans having social objectives:

- Over one third of the SLLs sampled had both social and environmental objectives

- The SLLs had specific social targets linked to equitable livelihood, as well as the creation of jobs and apprenticeships; quality of education; screening of suppliers on social-environmental factors; affordable housing, community engagement and development; diversity and inclusion promotion; and the eradication of homelessness.

- Governance-related objectives were still lagging, with only 14% of our SLL sample having E, S, and G goals.

Building an effective operating model

The issuance of SLLs, as well as other sustainable debt products, will continue to increase, as will the regulatory and public scrutiny placed on the performance of these instruments against their objectives.

Financial institutions should look to upskill their front office by providing additional training to help them engage with their clients on ESG. This would allow them to evaluate, and potentially challenge, their clients’ transition plans and help meet their net zero ambitions.

To manage these risks, financial institutions need to create a robust second line of defence for greenwashing embedded into the risk framework and thus, complementing the existing work of compliance, reputational risk and credit risk teams, and environmental and social due diligence processes.

The assessment of a company’s performance is not once and done, it needs to be embedded into the annual review processes across the bank, feeding the bank's financed emissions baseline and projections.

Simultaneously, financial institutions will need to review their own claims systemically and rigorously, and those of their clients and counterparties.

To learn more about our research, please contact us here

References:

1 Intergovernmental Panel on Climate Change (IPCC). (2022). IPCC Explainer: Stopping Climate Change. Available at: https://eciu.net/analysis/infographics/ipcc-explainer-mitigation-climate-change [Accessed 02 December 2022]

2 South Pole (October 2022). Going green, then going dark – One in four companies are keeping quiet on science-based targets. Available at: https://www.southpole.com/news/going-green-then-going-dark [Accessed 16 November 2022].

3 Bloomberg NEF (2022). Bloomberg NEF. Available at: https://about.bnef.com/ [Accessed 01 November 2022]

4 UN PRI (July 2022). Sustainability-linked loans: A strong ESG commitment or a vehicle for greenwashing? Available at: https://www.unpri.org/pri-blog/sustainability-linked-loans-a-strong-esg-commitment-or-a-vehicle-for-greenwashing/10243.article [Accessed 01 November 2022]

5 Financial Conduct Authority (October 2022). Sustainability Disclosure Requirements (SDR) and investment labels. Available at: https://www.fca.org.uk/publication/consultation/cp22-20.pdf [Accessed 16 November 2022]

6 Financial Conduct Authority (October 2022). FCA proposes new rules to tackle greenwashing. Available at: https://www.fca.org.uk/news/press-releases/fca-proposes-new-rules-tackle-greenwashing [Accessed on 01 November 2022]

7 Australian Securities & Investment Commission (June 2022). How to avoid greenwashing when offering or promoting sustainability-related products. Available at: https://asic.gov.au/regulatory-resources/financial-services/how-to-avoid-greenwashing-when-offering-or-promoting-sustainability-related-products/ [Accessed 16 November 2022].

Related Insights

From pledges to action: why Australian transition plans need a reset

The world has shifted since net zero targets were set. Discover why transition plans need a reset, and what leaders should do next.

Read more

Future-proofing climate disclosures: Leveraging climate reporting for nature

Forward-thinking companies are integrating climate and nature into their strategies to drive innovation and resilience.

Read more

Transition planning in turbulent times: How financial institutions can adapt and lead

The shift to a low-carbon economy is challenging for financial institutions; we explore how they can adapt and lead in today's tough landscape.

Read more

Simplification Omnibus: what you need to know and where to go from here

We share what the Simplification Omnibus means for CSRD, CS3D and the EU Taxonomy and how you should respond.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?