Measuring progress with purpose: a better approach to ESG data

12 August 2022

Understanding ESG challenges and solutions in financial services begins with making a vital distinction between ‘sustainability’ and ‘ESG’. While sustainability is the process of future-proofing the system we live in, ESG is about creating fit-for-purpose approaches to measuring progress against investment activities that can enable a sustainable economy. But too often, firms measure ESG impacts and risks as a tick-box, rather than measuring under a corporate purpose in line with social and environmental prosperity. Before ESG reporting is standardised, financial institutions have an opportunity to build purpose-led approaches to measuring ESG outcomes.

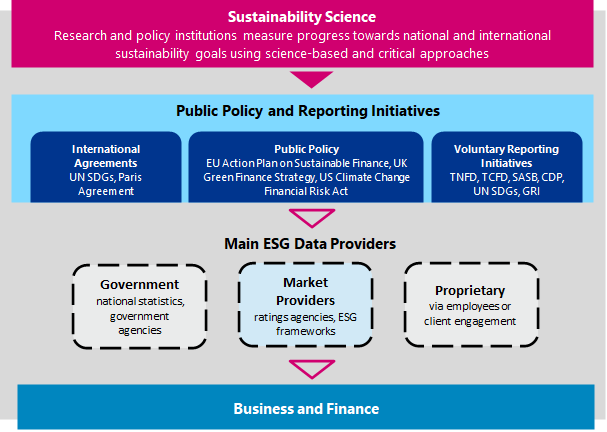

The ESG data system is not yet fit for purpose

ESG is just one cog in the wheel of sustainability. While sustainability is a principle by which organisations and systems can embed to ensure positive outcomes for society and nature, ESG is a means of gauging our progress in doing so. By measuring the real-world impacts and potential risks resulting from investment and lending decisions with transparent and accurate use of ESG metrics and targets, ESG can serve sustainability goals. And crucially, the impact that ESG approaches set out to measure must be increasingly positive. A key obstacle to this, however, is that the use of ESG data currently follows a dangerous trend in which sustainability is measured without a defined purpose and strategy. Although accurate and transparent information lies at the heart of effective financial decisions, the financial services industry relies on a nascent ESG data system backed by inconsistent standards and methodologies. This amount to three key challenges for the industry:

-

From measuring emissions to… everything else. Thanks to the GHG Protocol (and more recently PCAF), financial institutions can access or estimate publicly listed company emissions to arrive at relatively usable datasets. Beyond emissions data for listed companies, however, sourcing robust ESG data is difficult. Data gaps persist in the areas of biodiversity, resource depletion, circularity and social impact due to non-standardised and regionally concentrated reporting standards. At its foundation, financial institutions and the clients they serve suffer from insufficient flows of information from vital sources, and lack the necessary understanding, metrics and approaches to assess sustainability properly.

-

Oversimplification. Under efforts to overcome complexity, a common but flawed solution to creating decision useful ESG information is the aggregation of environmental, social and corporate governance factors into single data points. For example, the overall approach for ESG ratings holds promise by simplifying indicators into digestible and comparable metrics, in the same way creditworthiness is based on financial and operational indicators. But gross variation between ESG ratings among providers show that ratings currently lack the necessary data on underlying environmental and social capital, allowing the inevitable trade-offs between real-world sustainability impact to be overlooked. Research by CFA institute showed gross miscorrelation of company ESG ratings between top providers (including MSCI, Bloomberg and S&P), with only 5 of 30 comparisons showed a correlation above 50%. Equally, using a single ESG data point in structures such as SLLs limits the real-world positive impact of ‘sustainable’ products. Ultimately, sustainability cannot be boiled down into one ESG metric: the way sustainability impacts businesses and communities is complex by nature and avoiding this reality amounts to a lens that is narrow at best and dishonest at worst.

-

Greenwashing. The risks arising from intentional and unintentional greenwashing are higher than ever, as shown by BaFin’s crackdown on DWS and the SEC’s ruling and fine against BNY Mellon. While incoming regulation marks the boundaries of what is green and sustainable, its adoption by regulators shows zero tolerance towards greenwashing going forward. It also demonstrates a need to consider what incoming regulation means for legacy financing. Finance must now increasingly back up claims with data and evidence to credibly show that investment and lending decisions support sustainable activities.

Amidst widespread gaps in data and capability, increased risk from greenwashing or ‘sustainability-washing’, it is no longer feasible for financial institutions and their clients to ‘do’ ESG as a tick-box exercise. This means that the misuse and misrepresentation of ESG data creates a risk for users, underlining the need to develop credible solutions to measuring ESG outcomes backed by purpose.

Four principles for success in ESG data programmes

-

Use corporate purpose to define the right scope of ESG impact. Navigating towards an outcome which embraces sustainability begins with defining purpose – ‘a clear understanding of what the organisation can do and chooses to do about what they both care about and are positioned to do to contribute to a better society’ (Blueprint for Better Business). Developing a unique purpose allows organisations to scope the ESG factors most relevant to them, which can in turn be used to inform data requirements. The principle here is taking a focused approach to measuring impact and accepting the inevitability of data gaps and trade-offs between ESG factors with a clear strategy to navigate these.

-

Design a Data Architecture which caters to purpose and ESG requirements. A fit-for-purpose ESG dataset should align to the requirements and purpose of the organisation’s ESG strategy, and a purpose-driven data framework will identify trade-offs between ESG factors and key data gaps with a strategy to resolve these. Under a nascent ESG data system, practical questions from a business-value perspective become vital: ‘in the absence of company-level data, what alternative datasets are available to aid proxies and assumptions?’; ‘how material are the data gaps to our purpose and strategy?’; and ‘how does our data programme handle the changing scope of ESG regulations and trends?’. Ensuring that data availability and data quality meets business requirements requires sustainability capability across functions to ensure the right information is sourced and utilised.

-

Engage clients on sustainability. Financial institutions are empowered to improve the ESG data ecosystem by initiating and maintaining client conversations about sustainability to support information flows. Engagement on the disclosure of climate transition plans (including LGIM’s Climate Impact Pledge) has proven highly impactful to improve public and proprietary information – albeit amongst larger entities. Elsewhere, Lloyds Banking Group’s Sustainable Agriculture strategy encourages clients to measure farm emissions and resource use, based on a strengthened knowledge flow between the business and front office relationship managers trained in sustainability. Here, financial institutions can expand the remit of net zero processes to include sustainability.

-

Foster appropriate governance of sustainability. Fundamentally, governance is central to the development of purpose in line with sustainable outcomes and ensuring this follows through across operations. A key role for governance is to build the internal capabilities to recognise and reconcile the data gaps and tensions that emerge in ESG factors. Governance functions will need to engage with both internal employees to galvanise sustainability within operations, as well as build external partnerships to ensure knowledge sharing. Transition finance, for example, is an area which requires new decision-making frameworks at portfolio level to align with climate risk appetite and above all, a north-star purpose communicated by governance.

Towards a credible and purpose-led data approach

The ESG data system is nascent, but rather than discarding it we should seek to improve it. Organisations with a credible, purpose-led and data-driven approach to sustainability will succeed in today’s new ESG landscape. Against heightened regulatory and reputational risks, stand-out approaches to ESG data in finance are defined by determination in sourcing data and willingness to navigate data gaps creatively.

Want to know more about how to approach to ESG data management? Contact Paul Jones and Charlie Worsley.

-

Related Insights

Future-proofing climate disclosures: Leveraging climate reporting for nature

Forward-thinking companies are integrating climate and nature into their strategies to drive innovation and resilience.

Read more

Transition planning in turbulent times: How financial institutions can adapt and lead

The shift to a low-carbon economy is challenging for financial institutions; we explore how they can adapt and lead in today's tough landscape.

Read more

Simplification Omnibus: what you need to know and where to go from here

We share what the Simplification Omnibus means for CSRD, CS3D and the EU Taxonomy and how you should respond.

Read more

2025 Outlook: What lies ahead for climate and sustainability in financial services?

Here's what's front of our minds for 2025 based on our dialogue with, and work for, climate and sustainability leaders across financial institutions.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?